1. Introduction

On a stochastic basis

$(\Omega, \mathcal{F}, {\mathbb{P}};\; \mathbb{F})$

, where

$(\Omega, \mathcal{F}, {\mathbb{P}};\; \mathbb{F})$

, where

$\mathbb{F}=(\mathcal{F}_t)_{t\ge 0}$

is a (right-continuous) filtration, we consider a spectrally negative Lévy process

$\mathbb{F}=(\mathcal{F}_t)_{t\ge 0}$

is a (right-continuous) filtration, we consider a spectrally negative Lévy process

$X=(X_t)_{t\ge 0}$

starting at

$X=(X_t)_{t\ge 0}$

starting at

$x\in \mathbb{R}$

,

$x\in \mathbb{R}$

,

\begin{align*}X_t = x + ct + \sigma W_t - L_t,\quad t\ge 0,\end{align*}

\begin{align*}X_t = x + ct + \sigma W_t - L_t,\quad t\ge 0,\end{align*}

where

$x,c\in \mathbb{R}$

are constants,

$x,c\in \mathbb{R}$

are constants,

$W=(W_t)_{t\ge 0}$

is an

$W=(W_t)_{t\ge 0}$

is an

$\mathbb{F}$

-Wiener process, and

$\mathbb{F}$

-Wiener process, and

$L=(L_t)_{t\ge 0}$

is an

$L=(L_t)_{t\ge 0}$

is an

$\mathbb{F}$

-Lévy subordinator (possibly of infinite activity) with the Lévy measure

$\mathbb{F}$

-Lévy subordinator (possibly of infinite activity) with the Lévy measure

$\nu$

on

$\nu$

on

$(0,\infty)$

satisfying

$(0,\infty)$

satisfying

\begin{align*}\int_0^1 z\,\nu(\mathrm{d} z) < \infty,\quad \nu([1,\infty)) < \infty.\end{align*}

\begin{align*}\int_0^1 z\,\nu(\mathrm{d} z) < \infty,\quad \nu([1,\infty)) < \infty.\end{align*}

Note that

$W_0=L_0=0$

a.s. The Laplace exponent of X is defined as

$W_0=L_0=0$

a.s. The Laplace exponent of X is defined as

\begin{align*}\psi_X(\theta) \;:\!=\; \log \mathbb{E}[{\mathrm{e}}^{\theta (X_1 - x)}] = c\theta + \dfrac{\sigma^2}{2} \theta^2 +\int_0^\infty ({\mathrm{e}}^{-\theta z} -1)\,\nu(\mathrm{d} z),\quad \theta \ge 0.\end{align*}

\begin{align*}\psi_X(\theta) \;:\!=\; \log \mathbb{E}[{\mathrm{e}}^{\theta (X_1 - x)}] = c\theta + \dfrac{\sigma^2}{2} \theta^2 +\int_0^\infty ({\mathrm{e}}^{-\theta z} -1)\,\nu(\mathrm{d} z),\quad \theta \ge 0.\end{align*}

We are interested in the q-scale function of X,

$W^{(q)}\colon \mathbb{R}\to \mathbb{R}_+\;:\!=\; [0,\infty)$

for some

$W^{(q)}\colon \mathbb{R}\to \mathbb{R}_+\;:\!=\; [0,\infty)$

for some

$q\ge 0$

, defined as follows:

$q\ge 0$

, defined as follows:

$W^{(q)}(x) = 0$

on

$W^{(q)}(x) = 0$

on

$(\!-\!\infty,0)$

and otherwise

$(\!-\!\infty,0)$

and otherwise

$W^{(q)}$

is the unique continuous function that is right-continuous at the origin with the Laplace transform

$W^{(q)}$

is the unique continuous function that is right-continuous at the origin with the Laplace transform

\begin{align*}\int_0^\infty {\mathrm{e}}^{-\theta z}W^{(q)}(z)\,\mathrm{d} z = \dfrac{1}{\psi_X(\theta) - q}\quad \text{for $\theta > \Phi(q)$},\end{align*}

\begin{align*}\int_0^\infty {\mathrm{e}}^{-\theta z}W^{(q)}(z)\,\mathrm{d} z = \dfrac{1}{\psi_X(\theta) - q}\quad \text{for $\theta > \Phi(q)$},\end{align*}

where

$\Phi(q)$

is called the Lundberg exponent:

$\Phi(q)$

is called the Lundberg exponent:

\begin{align*}\Phi(q) \;:\!=\; \sup\{\theta \ge 0 \mid \psi_X(\theta) = q\}.\end{align*}

\begin{align*}\Phi(q) \;:\!=\; \sup\{\theta \ge 0 \mid \psi_X(\theta) = q\}.\end{align*}

The scale functions play essential roles in fluctuation theory of Lévy processes and have various applications in insurance and finance. For example, defining two stopping times

$\tau_\alpha^+=\inf\{t>0 \mid X_t>\alpha\}$

and

$\tau_\alpha^+=\inf\{t>0 \mid X_t>\alpha\}$

and

$\tau_\alpha^- = \inf\{t>0 \mid X_t < \alpha\}$

for each

$\tau_\alpha^- = \inf\{t>0 \mid X_t < \alpha\}$

for each

$\alpha\in \mathbb{R}$

, we have a fluctuation identity for

$\alpha\in \mathbb{R}$

, we have a fluctuation identity for

$a>0$

such that

$a>0$

such that

\begin{align*}\mathbb{E}\bigl[{\mathrm{e}}^{-q \tau_a^+}\boldsymbol{1}_{\{\tau_a^+ < \tau_0^-\}}\bigr] = \dfrac{W^{(q)}(x)}{W^{(q)}(a)} \quad \mbox{for $x \in [0,a]$},\end{align*}

\begin{align*}\mathbb{E}\bigl[{\mathrm{e}}^{-q \tau_a^+}\boldsymbol{1}_{\{\tau_a^+ < \tau_0^-\}}\bigr] = \dfrac{W^{(q)}(x)}{W^{(q)}(a)} \quad \mbox{for $x \in [0,a]$},\end{align*}

which is an essential identity in the theory of two-sided exit problems and useful in analyzing credit risks and barrier options, among others. As

$q=0$

, we have

$q=0$

, we have

${\mathbb{P}}(\tau_0^- <\tau_a^+) = 1 - W^{(0)}(x)/W^{(0)}(a)$

, and so assuming that

${\mathbb{P}}(\tau_0^- <\tau_a^+) = 1 - W^{(0)}(x)/W^{(0)}(a)$

, and so assuming that

\begin{align*}\psi'(0+) = c - \int_0^\infty z\,\nu(\mathrm{d} z) >0,\end{align*}

\begin{align*}\psi'(0+) = c - \int_0^\infty z\,\nu(\mathrm{d} z) >0,\end{align*}

called the net profit condition in ruin theory, which implies that

$W^{(0)}(\infty) = 1/\psi'(0+)$

, we have the well-known identity for the ruin probability in classical ruin theory:

$W^{(0)}(\infty) = 1/\psi'(0+)$

, we have the well-known identity for the ruin probability in classical ruin theory:

\begin{align}{\mathbb{P}}(\tau_0^- < \infty) = 1 - \psi'(0+)W^{(0)}(x). \end{align}

\begin{align}{\mathbb{P}}(\tau_0^- < \infty) = 1 - \psi'(0+)W^{(0)}(x). \end{align}

See Kyprianou [Reference Kyprianou14] for details regarding these identities. Moreover, Biffis and Kyprianou [Reference Biffis and Kyprianou5], as well as Feng and Shimizu [Reference Feng and Shimizu9], demonstrated that scale functions are useful tools for representing more general ruin-related risks. They showed that certain generalized Gerber–Shiu functions – whose classical version was introduced by Gerber and Shiu [Reference Gerber and Shiu10] – can also be expressed in terms of q-scale functions.

Scale functions also play a significant role in optimal dividend problems; see Loeffen [Reference Loeffen17]. Additionally, they are involved in the study of Parisian ruin probabilities, as explored by Loeffen et al. [Reference Loeffen, Czarna and Palmowski18] and Baurdoux et al. [Reference Baurdoux, Pardo, Perez and Renaud1], among others.

The connection between ruin theory and q-scale functions is deeply rooted in the potential theory of spectrally negative Lévy processes and the Wiener–Hopf factorization; see e.g. Bertoin [Reference Bertoin3, Reference Bertoin4] and Roger [Reference Roger20]. For further details, the reference lists in Kyprianou [Reference Kyprianou14], Kyprianou and Rivero [Reference Kyprianou and Rivero15], Feng and Shimizu [Reference Feng and Shimizu9], and Kuznetsov et al. [Reference Kuznetsov, Kyprianou and Rivero13] provide useful historical context and insights into their applications across various fields.

In considering such an application, it is important to recognize the practical need to identify the scale function and estimate it statistically from observations of a given Lévy process. Indeed, the identification and approximation of scale functions have attracted considerable attention in recent years.

We can find an explicit representation for some simple cases, such as compound Poisson processes; see e.g. Hubalek and Kyprianou [Reference Hubalek and Kyprianou11]. However, obtaining a general representation via the Laplace transform is generally challenging because Laplace inversion is too difficult to implement. Therefore, attempts have been made to obtain an approximate representation. The earliest work on an approximation of scale functions is due to Egami and Yamazaki [Reference Egami and Yamazaki8], who constructed an approximate sequence of q-scale functions using a compound Poisson-type Lévy process with phase-type jumps, forming a dense family in the class of spectrally negative Lévy processes. Landrault and Willmot [Reference Landrault and Willmot16] proposed an asymptotic expansion for Wiener–Poisson risk models by inverting the Laplace transform of scale functions and investigating some examples where explicit expansions are obtained. Behme et al. [Reference Behme, Oechsler and Schilling2] extended their results to more general Lévy processes with infinite jumps. Moreover, Xie et al. [Reference Xie, Cui and Zhang27] focused on a specific probabilistic representation of the q-scale function and provided an approximation formula using a Laguerre series expansion. See also Martín-González et al. [Reference Martín-González, Murillo-Salas and Pantí19] for an alternative expansion, and Surya [Reference Surya25] for numerical methods, among others.

Thus there are many discussions on the approximation of scale functions, but to the best of our knowledge, statistical inference based on underlying data has not yet been discussed. Our paper’s novelty lies not only in providing a new series approximation of the q-scale function but also a data-based statistical estimation of it. Among these, we are particularly concerned with problems in insurance actuarial practice. In modern actuarial practice, it is standard to use the spectrally negative Lévy process

$X=(X_t)_{t\ge 0}$

for the surplus or asset processes of insurance companies, and certain discrete observations of X are available as real data; see Section 3.1. However, it is usually not clear from the data which Lévy process these data follow. We therefore propose a method for estimating scale functions without specifying a model of X, by using a non-parametric method for estimating quantities associated with the Lévy measure.

$X=(X_t)_{t\ge 0}$

for the surplus or asset processes of insurance companies, and certain discrete observations of X are available as real data; see Section 3.1. However, it is usually not clear from the data which Lévy process these data follow. We therefore propose a method for estimating scale functions without specifying a model of X, by using a non-parametric method for estimating quantities associated with the Lévy measure.

We must take two steps to identify the q-scale function in practice. First we introduce a new approximation formula. We focus on a compound geometric integral representation of the q-scale function obtained by Feng and Shimizu [Reference Feng and Shimizu9]. We derive a Laguerre series expansion of the corresponding compound geometric distribution function, and the Stieltjes integral with respect to it gives the expansion of the q-scale function. Although we also use a Laguerre expansion, as in Xie et al. [Reference Xie, Cui and Zhang27], our approach differs from theirs, and the formula is fundamentally different, which constitutes the primary contribution of this paper.

Second, we proceed to statistical inference. Two studies, by Zhang and Su [Reference Zhang and Su29] and Shimizu and Zhang [Reference Shimizu and Zhimin24], are instructive in this regard. The former proposes an estimator of Gerber–Shiu functions by deriving its Laguerre series expansion and estimating the coefficients for each term. They show the consistency of their proposed estimator. Shimizu and Zhang [Reference Shimizu and Zhimin24] applied the same approach to ruin probability and further showed that the estimator is asymptotically normal. As shown in equation (1.1), the ruin probability is represented by

$W^{(0)}(x)$

, so their estimator is also an asymptotically normal estimator for the 0-scale function. This paper constructs an asymptotically normal estimator of the q-scale function, which generalizes the results of [Reference Shimizu and Zhimin24].

$W^{(0)}(x)$

, so their estimator is also an asymptotically normal estimator for the 0-scale function. This paper constructs an asymptotically normal estimator of the q-scale function, which generalizes the results of [Reference Shimizu and Zhimin24].

The paper is organized as follows. Section 2 introduces the series representation of the q-scale function obtained by Feng and Shimizu [Reference Feng and Shimizu9]. Under the net profit condition, the q-scale function has an integral representation in the form of the expected value of the compound geometric distribution. Section 3 covers statistical inference. Assuming X to be a surplus model, we construct auxiliary statistics for each unknown parameter under a reasonable discrete observation scheme. Finally, in Section 3.2, we construct an estimator for the Laguerre expansion of the q-scale function based on these auxiliary statistics. The proposed estimators are shown to be consistent and asymptotically normal. Supplementary lemmas are summarized in the Appendix.

Notation. Throughout the paper, we use the following notation.

-

•

$\mathbb{N} = \{1,2,3,\ldots\}$

;

$\mathbb{N}_0\;:\!=\; \mathbb{N} \cup \{0\}$

;

$\mathbb{R}_+\;:\!=\; [0,\infty)$

.

$\mathbb{N} = \{1,2,3,\ldots\}$

;

$\mathbb{N}_0\;:\!=\; \mathbb{N} \cup \{0\}$

;

$\mathbb{R}_+\;:\!=\; [0,\infty)$

. -

• For a

$d\times d$

matrix

$A=(a_{ij})_{1\le i,j\le d}$

, let

$|A| \;:\!=\; \bigl( \sum_{i,j=1}^d a_{ij}^2 \bigr)^{1/2}$

. -

• For

$\boldsymbol{a}=(a_1,\ldots,a_d)^\top$

and

${\boldsymbol{b}}=(b_1,\ldots,b_d)^\top$

, the inner product is defined by

$\boldsymbol{a}\cdot {\boldsymbol{b}} =\sum_{k=1}^d a_kb_k$

. -

• Let

${\boldsymbol 0}_d$

denote the zero vector of dimension d, and let

$I_d$

be the

$d\times d$

identity matrix. Moreover,

$N_d(\boldsymbol{a}, \Sigma)$

denotes the d-dim Gaussian distribution with mean vector

$\boldsymbol{a}$

and covariance matrix

$\Sigma$

. In particular,

$N\;:\!=\; N_1$

. -

• The indicator function on a set

$A\subset \mathbb{R}$

is given by

$\boldsymbol{1}_A(x) = 1$

if

$x\in A$

; 0 otherwise. -

• For functions f, g on

$\mathbb{R}$

, let

$f(x) \lesssim g(x)$

if there exists a constant

$C>0$

such that

$f(x) \le C g(x)$

for any

$x\in \mathbb{R}$

. -

• For a function

$f(x_1,x_2,\ldots,x_d)$

, let

\begin{align*} \partial_{x_i} f \;:\!=\; \frac{\partial f}{\partial x_i}\quad\text{and}\quad \partial_{(x_1,\ldots,x_d)} f = (\partial_{x_1} f,\ldots, \partial_{x_d}f)^\top. \end{align*}

-

• For

$s\ge 1$

and

$\alpha>0$

, let In particular, we let

\begin{align*}L^s_\alpha(\mathbb{R}_+) = \biggl\{f\colon \mathbb{R}_+\to \mathbb{R}\,\colon \, \int_0^\infty f^s(x)\,{\mathrm{e}}^{-\alpha x}\,\mathrm{d} x < \infty \biggr\}.\end{align*}

$L^s(\mathbb{R}_+) \;:\!=\; L^s_0(\mathbb{R}_+)$

, and for

$f,g\in L^2(\mathbb{R}_+)$

,

\begin{align*}\langle f,g\rangle \;:\!=\; \int_0^\infty f(x)g(x)\,\mathrm{d} x,\quad \|f\|\;:\!=\; \sqrt{\langle f,f\rangle}.\end{align*}

-

• For functions f, g on

$\mathbb{R}_+$

of finite variation, the convolution is defined as Moreover, the kth convolution is defined by

\begin{align*}f*g (x) \;:\!=\; \int_{[0,x]}f(x-y)g(y)\,\mathrm{d} y,\quad x\ge 0.\end{align*}

$f^{*0}= \delta_0$

(Dirac’s delta function concentrated on 0) and

$f^{*k} = f*f^{*(k-1)}$

for

$k\in \mathbb{N}$

.

-

• For a measure

$\nu$

on

$\mathbb{R}_+$

and a function

${\boldsymbol{f}}=(f_1,\ldots,f_d)^\top\colon \mathbb{R}_+\to \mathbb{R}^d$

, we let

\begin{align*}\nu({\boldsymbol{f}}) \;:\!=\; \int_{\mathbb{R}_+} {\boldsymbol{f}}(x)\,\nu(\mathrm{d} x) = \biggl(\int_{\mathbb{R}_+} f_1(x)\,\nu(\mathrm{d} x),\ldots,\int_{\mathbb{R}_+} f_d(x)\,\nu(\mathrm{d} x)\biggr)^\top.\end{align*}

2. Series representation of q-scale functions

2.1. A compound geometric representation of q-scale functions

A closed-form expression for the q-scale function of the process X was derived by Feng and Shimizu [Reference Feng and Shimizu9] as an expectation with respect to a compound geometric distribution under the following net profit condition:

NPC

$\displaystyle c > \int_0^\infty z\,\nu(\mathrm{d} z)$

.

$\displaystyle c > \int_0^\infty z\,\nu(\mathrm{d} z)$

.

To state the representation of

$W^{(q)}$

, we prepare some notation. We will fix a number

$W^{(q)}$

, we prepare some notation. We will fix a number

$q\ge 0$

for

$q\ge 0$

for

$W^{(q)}$

, and let

$W^{(q)}$

, and let

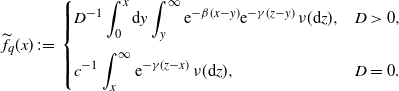

\begin{align*}D\;:\!=\; \dfrac{\sigma^2}{2},\quad \gamma\;:\!=\; \Phi(q),\quad\beta=\begin{cases}cD^{-1} + \gamma, & D>0, \\[5pt] \gamma, & D=0,\end{cases}\end{align*}

\begin{align*}D\;:\!=\; \dfrac{\sigma^2}{2},\quad \gamma\;:\!=\; \Phi(q),\quad\beta=\begin{cases}cD^{-1} + \gamma, & D>0, \\[5pt] \gamma, & D=0,\end{cases}\end{align*}

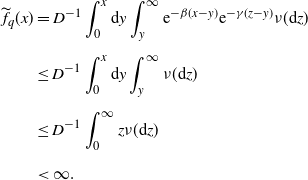

\begin{align*}\widetilde{f}_q(x) \;:\!=\;\begin{cases} \displaystyle D^{-1}\int_0^x \mathrm{d} y \int_y^{\infty} {\mathrm{e}}^{-\beta(x-y)}{\mathrm{e}}^{-\gamma(z-y)}\,\nu(\mathrm{d} z), & D > 0, \\[13pt] \displaystyle c^{-1}\int_x^{\infty} {\mathrm{e}}^{-\gamma(z-x)}\,\nu(\mathrm{d} z), & D=0.\end{cases} \end{align*}

\begin{align*}\widetilde{f}_q(x) \;:\!=\;\begin{cases} \displaystyle D^{-1}\int_0^x \mathrm{d} y \int_y^{\infty} {\mathrm{e}}^{-\beta(x-y)}{\mathrm{e}}^{-\gamma(z-y)}\,\nu(\mathrm{d} z), & D > 0, \\[13pt] \displaystyle c^{-1}\int_x^{\infty} {\mathrm{e}}^{-\gamma(z-x)}\,\nu(\mathrm{d} z), & D=0.\end{cases} \end{align*}

We define a distribution

$F_q$

with a probability density obtained from the function

$F_q$

with a probability density obtained from the function

$\widetilde{f}_q$

:

$\widetilde{f}_q$

:

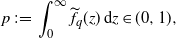

\begin{align*}F_q(x) \;:\!=\; \int_0^x f_q(z)\,\mathrm{d} z,\quad f_q(z) = p^{-1} \widetilde{f}_q(z),\quad p \;:\!=\; \int_0^\infty \widetilde{f}_q(z)\,\mathrm{d} z.\end{align*}

\begin{align*}F_q(x) \;:\!=\; \int_0^x f_q(z)\,\mathrm{d} z,\quad f_q(z) = p^{-1} \widetilde{f}_q(z),\quad p \;:\!=\; \int_0^\infty \widetilde{f}_q(z)\,\mathrm{d} z.\end{align*}

In fact,

$p\in (0,1)$

under the NPC condition and the probability density

$p\in (0,1)$

under the NPC condition and the probability density

$f_q$

is well-defined; see Lemma C.1. Then the following representation is the immediate consequence from Feng and Shimizu [Reference Feng and Shimizu9, Proposition 4.1].

$f_q$

is well-defined; see Lemma C.1. Then the following representation is the immediate consequence from Feng and Shimizu [Reference Feng and Shimizu9, Proposition 4.1].

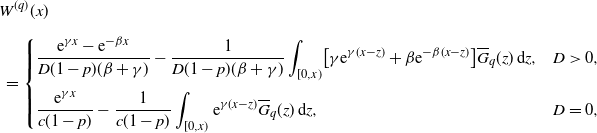

Lemma 2.1. Suppose the NPC condition for the process X. Then the q-scale function

$W^{(q)}$

of X has the following integral form:

$W^{(q)}$

of X has the following integral form:

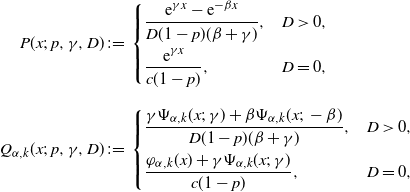

\begin{align*}& W^{(q)}(x) \\[5pt] &\ = \begin{cases} \displaystyle \dfrac{{\mathrm{e}}^{\gamma x} - {\mathrm{e}}^{-\beta x}}{D(1-p)(\beta+ \gamma)} - \dfrac{1}{D(1-p)(\beta+ \gamma)}\int_{[0,x)} \bigl[\gamma {\mathrm{e}}^{\gamma(x-z)} + \beta {\mathrm{e}}^{-\beta(x-z)}\bigr] \overline{G}_q(z)\,\mathrm{d} z, & D>0, \\[13pt] \displaystyle \dfrac{{\mathrm{e}}^{\gamma x}}{c(1-p)} - \dfrac{1}{c(1-p)}\int_{[0,x)} {\mathrm{e}}^{\gamma(x-z)}\overline{G}_q(z)\,\mathrm{d} z, & D=0,\end{cases} \end{align*}

\begin{align*}& W^{(q)}(x) \\[5pt] &\ = \begin{cases} \displaystyle \dfrac{{\mathrm{e}}^{\gamma x} - {\mathrm{e}}^{-\beta x}}{D(1-p)(\beta+ \gamma)} - \dfrac{1}{D(1-p)(\beta+ \gamma)}\int_{[0,x)} \bigl[\gamma {\mathrm{e}}^{\gamma(x-z)} + \beta {\mathrm{e}}^{-\beta(x-z)}\bigr] \overline{G}_q(z)\,\mathrm{d} z, & D>0, \\[13pt] \displaystyle \dfrac{{\mathrm{e}}^{\gamma x}}{c(1-p)} - \dfrac{1}{c(1-p)}\int_{[0,x)} {\mathrm{e}}^{\gamma(x-z)}\overline{G}_q(z)\,\mathrm{d} z, & D=0,\end{cases} \end{align*}

where

$p\in (0,1)$

and

$p\in (0,1)$

and

$G_q$

is a compound geometric distribution function

$G_q$

is a compound geometric distribution function

\begin{align}G_q(x) = \sum_{k=0}^\infty (1-p)p^k \int_0^x f_q^{*k}(z)\,\mathrm{d} z,\quad x\ge 0, \end{align}

\begin{align}G_q(x) = \sum_{k=0}^\infty (1-p)p^k \int_0^x f_q^{*k}(z)\,\mathrm{d} z,\quad x\ge 0, \end{align}

and

$G_q(x)\equiv 0$

for

$G_q(x)\equiv 0$

for

$x<0$

.

$x<0$

.

Proof. See Section C.4.

2.2. Laguerre series expansion

Let

$L_k(x)$

be the Laguerre polynomial of order k,

$L_k(x)$

be the Laguerre polynomial of order k,

\begin{align*}L_k(x) = \dfrac{1}{n!}{\mathrm{e}}^x \dfrac{\mathrm{d}^n}{\mathrm{d} x^n} ({\mathrm{e}}^{-x}x^n) = \sum_{j=0}^k \binom{k}{j} \dfrac{(\!-\!x)^j}{j!}, \quad x\in \mathbb{R}_+\;:\!=\; [0,\infty),\end{align*}

\begin{align*}L_k(x) = \dfrac{1}{n!}{\mathrm{e}}^x \dfrac{\mathrm{d}^n}{\mathrm{d} x^n} ({\mathrm{e}}^{-x}x^n) = \sum_{j=0}^k \binom{k}{j} \dfrac{(\!-\!x)^j}{j!}, \quad x\in \mathbb{R}_+\;:\!=\; [0,\infty),\end{align*}

by which we define the Laguerre function for each

$\alpha>0$

as follows:

$\alpha>0$

as follows:

\begin{align*}\varphi_{\alpha,k}(x) \;:\!=\; \sqrt{2\alpha}L_k(2\alpha x) \,{\mathrm{e}}^{-\alpha x},\quad x\in \mathbb{R}_+.\end{align*}

\begin{align*}\varphi_{\alpha,k}(x) \;:\!=\; \sqrt{2\alpha}L_k(2\alpha x) \,{\mathrm{e}}^{-\alpha x},\quad x\in \mathbb{R}_+.\end{align*}

Note that the system

$\{\varphi_{\alpha,k}\}_{k\in \mathbb{N}_0}$

consists of an orthogonal basis of

$\{\varphi_{\alpha,k}\}_{k\in \mathbb{N}_0}$

consists of an orthogonal basis of

$L^2(\mathbb{R}_+)$

satisfying

$L^2(\mathbb{R}_+)$

satisfying

\begin{align}\sup_{k\in \mathbb{N}_0,x\in \mathbb{R}_+}|\varphi_{\alpha,k}(x)|\le \sqrt{2\alpha }, \end{align}

\begin{align}\sup_{k\in \mathbb{N}_0,x\in \mathbb{R}_+}|\varphi_{\alpha,k}(x)|\le \sqrt{2\alpha }, \end{align}

and that for any

$k\in \mathbb{N}_0$

, there exists some

$k\in \mathbb{N}_0$

, there exists some

$\delta>0$

such that

$\delta>0$

such that

\begin{align*}\varphi_{\alpha,k}(x) = {\mathrm{O}} \big({\mathrm{e}}^{-(\alpha - \delta)x}\big),\quad x\to \infty,\end{align*}

\begin{align*}\varphi_{\alpha,k}(x) = {\mathrm{O}} \big({\mathrm{e}}^{-(\alpha - \delta)x}\big),\quad x\to \infty,\end{align*}

since

$L_k$

is a polynomial of order k. Therefore we can control the decay order of the function

$L_k$

is a polynomial of order k. Therefore we can control the decay order of the function

$\varphi_{k,\alpha}$

by choosing

$\varphi_{k,\alpha}$

by choosing

$\alpha>0$

; see Remark 2.1.

$\alpha>0$

; see Remark 2.1.

Let

$\mathcal{W}_\alpha^r(\mathbb{R}_+)$

be the Sobolev–Laguerre space (Bongioanni and Torrea [Reference Bongioanni and Torrea6]) for

$\mathcal{W}_\alpha^r(\mathbb{R}_+)$

be the Sobolev–Laguerre space (Bongioanni and Torrea [Reference Bongioanni and Torrea6]) for

$\alpha, r>0$

:

$\alpha, r>0$

:

\begin{align*}\mathcal{W}_\alpha^r(\mathbb{R}_+) \;:\!=\; \Biggl\{ f\in L^2(\mathbb{R}_+) \colon \sum_{k=0}^\infty k^r |\langle f,\varphi_{\alpha,k}\rangle|^2 < \infty\Biggr\}.\end{align*}

\begin{align*}\mathcal{W}_\alpha^r(\mathbb{R}_+) \;:\!=\; \Biggl\{ f\in L^2(\mathbb{R}_+) \colon \sum_{k=0}^\infty k^r |\langle f,\varphi_{\alpha,k}\rangle|^2 < \infty\Biggr\}.\end{align*}

There are many useful connections between Laguerre systems and the Sobolev–Laguerre space, as discussed in Comte and Genon-Catalot [Reference Comte and Genon-Catalot7]. In particular, Proposition 7.1 and its remark provide an equivalent condition for a function to belong to

$\mathcal{W}_\alpha^r(\mathbb{R}_+)$

, as follows.

$\mathcal{W}_\alpha^r(\mathbb{R}_+)$

, as follows.

Lemma 2.2. (Comte and Genon-Catalot [Reference Comte and Genon-Catalot7].) Let

$r\in \mathbb{N}$

and

$r\in \mathbb{N}$

and

$\alpha>0$

. Then

$\alpha>0$

. Then

$f\in \mathcal{W}_\alpha^r(\mathbb{R}_+)$

if and only if f admits the derivatives of order r and that

$f\in \mathcal{W}_\alpha^r(\mathbb{R}_+)$

if and only if f admits the derivatives of order r and that

\begin{align}x^{m/2} \partial_x^m f(x) \in L^2_\alpha(\mathbb{R}_+),\quad 0\le m\le r. \end{align}

\begin{align}x^{m/2} \partial_x^m f(x) \in L^2_\alpha(\mathbb{R}_+),\quad 0\le m\le r. \end{align}

The following uniform convergence of the Laguerre series expansion is obtained by Shimizu and Zhang [Reference Shimizu and Zhimin24, Proposition 3].

Lemma 2.3. For any

$K\in \mathbb{N}$

, the partial sum of the Laguerre series expansion of

$K\in \mathbb{N}$

, the partial sum of the Laguerre series expansion of

$f\in \mathcal{W}_\alpha^r(\mathbb{R}_+)$

,

$f\in \mathcal{W}_\alpha^r(\mathbb{R}_+)$

,

\begin{align*}f_K(x)\;:\!=\; \sum_{k=0}^K \langle f,\varphi_{\alpha,k}\rangle \varphi_{\alpha,k}(x),\quad x\ge 0,\end{align*}

\begin{align*}f_K(x)\;:\!=\; \sum_{k=0}^K \langle f,\varphi_{\alpha,k}\rangle \varphi_{\alpha,k}(x),\quad x\ge 0,\end{align*}

satisfies

\begin{align*}\sup_{x\in \mathbb{R}_+} |f_K(x) - f(x)| = {\mathrm{O}}(K^{-(r-1)/2}),\quad K\to \infty.\end{align*}

\begin{align*}\sup_{x\in \mathbb{R}_+} |f_K(x) - f(x)| = {\mathrm{O}}(K^{-(r-1)/2}),\quad K\to \infty.\end{align*}

2.3. Laguerre expansion of

$\overline{\boldsymbol{G}}_{\boldsymbol{q}}$

According to Willmot and Lin [Reference Willmot and Lin26], for example, we see that the tail function

$\overline{G}_q\;:\!=\; 1 - G_q$

should satisfy the following defective renewal equation (DRE):

$\overline{G}_q\;:\!=\; 1 - G_q$

should satisfy the following defective renewal equation (DRE):

\begin{align} \overline{G}_q(x) = p\overline{F}_q + pf_q(x)* \overline{G}_q(x),\quad x\ge 0. \end{align}

\begin{align} \overline{G}_q(x) = p\overline{F}_q + pf_q(x)* \overline{G}_q(x),\quad x\ge 0. \end{align}

We have the Laguerre expansion of

$pf_q$

,

$pf_q$

,

$p\overline{F}_q$

, and

$p\overline{F}_q$

, and

$\overline{G}_q$

since these belong to

$\overline{G}_q$

since these belong to

$L^2(\mathbb{R}_+)$

as shown in Section C.1: for

$L^2(\mathbb{R}_+)$

as shown in Section C.1: for

$x\ge 0$

,

$x\ge 0$

,

\begin{align*}pf_{q}(x)=\sum_{k=0}^{\infty}a^{f}_{\alpha,k}\varphi_{\alpha,k}(x),\quad p\overline{F}_{q}(x)=\sum_{k=0}^{\infty}a^{F}_{\alpha,k}\varphi_{\alpha,k}(x),\quad\overline{G}_{q}(x)=\sum_{k=0}^{\infty}a^{G}_{\alpha,k}\varphi_{\alpha,k}(x), \end{align*}

\begin{align*}pf_{q}(x)=\sum_{k=0}^{\infty}a^{f}_{\alpha,k}\varphi_{\alpha,k}(x),\quad p\overline{F}_{q}(x)=\sum_{k=0}^{\infty}a^{F}_{\alpha,k}\varphi_{\alpha,k}(x),\quad\overline{G}_{q}(x)=\sum_{k=0}^{\infty}a^{G}_{\alpha,k}\varphi_{\alpha,k}(x), \end{align*}

where

$a^{f}_{\alpha,k}\;:\!=\; \langle pf_{q}, \varphi_{\alpha,k}\rangle$

,

$a^{f}_{\alpha,k}\;:\!=\; \langle pf_{q}, \varphi_{\alpha,k}\rangle$

,

$a^{F}_{\alpha,k}\;:\!=\; \langle p\overline{F}_{q}, \varphi_{\alpha,k}\rangle$

, and

$a^{F}_{\alpha,k}\;:\!=\; \langle p\overline{F}_{q}, \varphi_{\alpha,k}\rangle$

, and

$a^{G}_{\alpha,k}\;:\!=\; \langle \overline{G}_{q}, \varphi_{\alpha,k}\rangle$

.

$a^{G}_{\alpha,k}\;:\!=\; \langle \overline{G}_{q}, \varphi_{\alpha,k}\rangle$

.

For arbitrary

$K\in \mathbb{N}_0$

, letting

$K\in \mathbb{N}_0$

, letting

\begin{align*}\boldsymbol{a}^{f}_{\alpha,K}&\;:\!=\; \bigl(a^{f}_{\alpha,0},a^{f}_{\alpha,1},\ldots,a^{f}_{\alpha,K}\bigr)^{\top}, \\[5pt] \boldsymbol{a}^{F}_{\alpha,K}&\;:\!=\; \bigl(a^{F}_{\alpha,0},a^{F}_{\alpha,1},\ldots,a^{F}_{\alpha,K}\bigr)^{\top}, \\[5pt] \boldsymbol{a}^{G}_{\alpha,K}&\;:\!=\; \bigl(a^{G}_{\alpha,0},a^{G}_{\alpha,1},\ldots,a^{G}_{\alpha,K}\bigr)^{\top},\end{align*}

\begin{align*}\boldsymbol{a}^{f}_{\alpha,K}&\;:\!=\; \bigl(a^{f}_{\alpha,0},a^{f}_{\alpha,1},\ldots,a^{f}_{\alpha,K}\bigr)^{\top}, \\[5pt] \boldsymbol{a}^{F}_{\alpha,K}&\;:\!=\; \bigl(a^{F}_{\alpha,0},a^{F}_{\alpha,1},\ldots,a^{F}_{\alpha,K}\bigr)^{\top}, \\[5pt] \boldsymbol{a}^{G}_{\alpha,K}&\;:\!=\; \bigl(a^{G}_{\alpha,0},a^{G}_{\alpha,1},\ldots,a^{G}_{\alpha,K}\bigr)^{\top},\end{align*}

we have the following relation among these coefficients; see Zhang and Su [Reference Zhang and Su28, Section 2] or Shimizu and Zhang [Reference Shimizu and Zhimin24, Proposition 2].

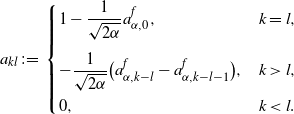

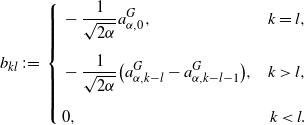

Lemma 2.4. Define a

$(K+1)\times(K+1)$

-matrix

$(K+1)\times(K+1)$

-matrix

$A^f_{K}=(a_{kl})_{1\le k,l\le K+1}$

, whose components are given as follows:

$A^f_{K}=(a_{kl})_{1\le k,l\le K+1}$

, whose components are given as follows:

\begin{align*} a_{kl}\;:\!=\; \begin{cases} 1-\dfrac{1}{\sqrt{2\alpha}}a^{f}_{\alpha,0}, &k=l,\\[13pt] -\dfrac{1}{\sqrt{2\alpha}}\bigl(a^{f}_{\alpha,k-l}-a^{f}_{\alpha,k-l-1}\bigr),&k>l,\\[7pt] 0,&k<l. \end{cases}\end{align*}

\begin{align*} a_{kl}\;:\!=\; \begin{cases} 1-\dfrac{1}{\sqrt{2\alpha}}a^{f}_{\alpha,0}, &k=l,\\[13pt] -\dfrac{1}{\sqrt{2\alpha}}\bigl(a^{f}_{\alpha,k-l}-a^{f}_{\alpha,k-l-1}\bigr),&k>l,\\[7pt] 0,&k<l. \end{cases}\end{align*}

Then the matrix

$A^f_K$

is invertible, and it holds that

$A^f_K$

is invertible, and it holds that

\begin{align*}\boldsymbol{a}^{G}_{\alpha,K}= \bigl(A^f_{K}\bigr)^{-1} \boldsymbol{a}^{F}_{\alpha,K}.\end{align*}

\begin{align*}\boldsymbol{a}^{G}_{\alpha,K}= \bigl(A^f_{K}\bigr)^{-1} \boldsymbol{a}^{F}_{\alpha,K}.\end{align*}

Using this system, we can construct a Laguerre expansion of

$\overline{G}_q(x)$

: for a vector

$\overline{G}_q(x)$

: for a vector

${\boldsymbol \varphi}_{\alpha,K} = (\varphi_{\alpha,0},\varphi_{\alpha,1},\ldots,\varphi_{\alpha,K})^\top$

,

${\boldsymbol \varphi}_{\alpha,K} = (\varphi_{\alpha,0},\varphi_{\alpha,1},\ldots,\varphi_{\alpha,K})^\top$

,

\begin{align}\overline{G}_{q,K}(x)\;:\!=\; \sum_{k=0}^K a_{\alpha,k}^G \varphi_{\alpha,k}(x) = \boldsymbol{a}^{G}_{\alpha,K}\cdot {\boldsymbol \varphi}_{\alpha,K} ,\quad x\in \mathbb{R}_+. \end{align}

\begin{align}\overline{G}_{q,K}(x)\;:\!=\; \sum_{k=0}^K a_{\alpha,k}^G \varphi_{\alpha,k}(x) = \boldsymbol{a}^{G}_{\alpha,K}\cdot {\boldsymbol \varphi}_{\alpha,K} ,\quad x\in \mathbb{R}_+. \end{align}

Lemma 2.5. Suppose the tail function of the Lévy measure

$\nu$

, say

$\nu$

, say

$\overline{\nu}(x)\;:\!=\; \int_x^\infty \nu(\mathrm{d} z)$

, admits derivatives up to order

$\overline{\nu}(x)\;:\!=\; \int_x^\infty \nu(\mathrm{d} z)$

, admits derivatives up to order

$r > 1$

and that the distribution

$r > 1$

and that the distribution

$G_q$

given in (2.1) has moments of any polynomial order. Moreover, suppose there exists a constant

$G_q$

given in (2.1) has moments of any polynomial order. Moreover, suppose there exists a constant

$\kappa>0$

such that

$\kappa>0$

such that

\begin{align}\partial_x^m \overline{\nu}(x) = {\mathrm{O}} (1 + x^\kappa), \quad x\to \infty, \end{align}

\begin{align}\partial_x^m \overline{\nu}(x) = {\mathrm{O}} (1 + x^\kappa), \quad x\to \infty, \end{align}

for any

$0\le m \le r-2$

. Then we have

$0\le m \le r-2$

. Then we have

$\overline{G}_q \in \mathcal{W}_\alpha^r(\mathbb{R}_+)$

, and therefore

$\overline{G}_q \in \mathcal{W}_\alpha^r(\mathbb{R}_+)$

, and therefore

\begin{align}\sup_{x\in \mathbb{R}_+}\bigl|\overline{G}_{q,K}(x) - \overline{G}_q(x)\bigr| = {\mathrm{O}} (K^{-(r-1)/2}) \to 0,\quad K\to \infty. \end{align}

\begin{align}\sup_{x\in \mathbb{R}_+}\bigl|\overline{G}_{q,K}(x) - \overline{G}_q(x)\bigr| = {\mathrm{O}} (K^{-(r-1)/2}) \to 0,\quad K\to \infty. \end{align}

Furthermore, if the condition (2.6) is much milder, such as

\begin{align}\partial_x^m \overline{\nu}(x) = {\mathrm{O}}( {\mathrm{e}}^{\kappa x}), \quad x\to \infty, \end{align}

\begin{align}\partial_x^m \overline{\nu}(x) = {\mathrm{O}}( {\mathrm{e}}^{\kappa x}), \quad x\to \infty, \end{align}

then the consequence (2.7) also holds if we choose

$\alpha > 2\kappa$

.

$\alpha > 2\kappa$

.

Proof. See Section C.5.

Remark 2.1. Lemma 2.5 explains the significance of the tuning parameter

$\alpha>0$

in the Laguerre function. When considering a model in which the Lévy measure satisfies (2.8), we can choose

$\alpha>0$

in the Laguerre function. When considering a model in which the Lévy measure satisfies (2.8), we can choose

$\alpha$

such that

$\alpha$

such that

$a>2\kappa$

. However, in most standard cases where (2.6) holds, we can choose any

$a>2\kappa$

. However, in most standard cases where (2.6) holds, we can choose any

$\alpha>0$

; in particular, setting

$\alpha>0$

; in particular, setting

$\alpha =1$

is both simple and sufficient.

$\alpha =1$

is both simple and sufficient.

2.4. Laguerre-type expansion for q-scale functions

We can obtain a series expansion of the q-scale function by replacing

$\overline{G}_q(z)$

in the expression of

$\overline{G}_q(z)$

in the expression of

$W^{(q)}$

in Lemma 2.1 with the corresponding Laguerre expansion (2.5).

$W^{(q)}$

in Lemma 2.1 with the corresponding Laguerre expansion (2.5).

Definition 2.1. For any

$K\in \mathbb{N}$

and

$K\in \mathbb{N}$

and

$\alpha>0$

, the Kth-Laguerre-type expansion of

$\alpha>0$

, the Kth-Laguerre-type expansion of

$W^{(q)}$

, say

$W^{(q)}$

, say

$W^{(q)}_K$

, is given by

$W^{(q)}_K$

, is given by

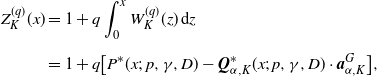

\begin{align}W^{(q)}_K(x) \;:\!=\; P(x;\;p,\gamma,D) - {\boldsymbol{Q}}_{\alpha,K}(x;\;p,\gamma,D)\cdot \boldsymbol{a}^G_{\alpha,K}, \end{align}

\begin{align}W^{(q)}_K(x) \;:\!=\; P(x;\;p,\gamma,D) - {\boldsymbol{Q}}_{\alpha,K}(x;\;p,\gamma,D)\cdot \boldsymbol{a}^G_{\alpha,K}, \end{align}

where

${\boldsymbol{Q}}_{\alpha,K}\;:\!=\; (Q_{\alpha,0}, Q_{\alpha,1},\ldots, Q_{\alpha,K})^\top$

with

${\boldsymbol{Q}}_{\alpha,K}\;:\!=\; (Q_{\alpha,0}, Q_{\alpha,1},\ldots, Q_{\alpha,K})^\top$

with

\begin{align*}P(x;\;p,\gamma,D)&\;:\!=\;\begin{cases} \dfrac{{\mathrm{e}}^{\gamma x}-{\mathrm{e}}^{-\beta x}}{D(1-p)(\beta+\gamma)},&D>0,\\[9pt] \dfrac{{\mathrm{e}}^{\gamma x}}{c(1-p)},&D=0,\end{cases} \\[9pt] Q_{\alpha,k}(x;\;p,\gamma,D)&\;:\!=\;\begin{cases} \dfrac{\gamma \Psi_{\alpha,k}(x;\;\gamma)+\beta\Psi_{\alpha,k}(x;\;-\beta)}{D(1-p)(\beta+\gamma)},&D>0,\\[9pt] \dfrac{\varphi_{\alpha,k}(x)+\gamma \Psi_{\alpha,k}(x;\;\gamma)}{c(1-p)},&D=0, \end{cases}\end{align*}

\begin{align*}P(x;\;p,\gamma,D)&\;:\!=\;\begin{cases} \dfrac{{\mathrm{e}}^{\gamma x}-{\mathrm{e}}^{-\beta x}}{D(1-p)(\beta+\gamma)},&D>0,\\[9pt] \dfrac{{\mathrm{e}}^{\gamma x}}{c(1-p)},&D=0,\end{cases} \\[9pt] Q_{\alpha,k}(x;\;p,\gamma,D)&\;:\!=\;\begin{cases} \dfrac{\gamma \Psi_{\alpha,k}(x;\;\gamma)+\beta\Psi_{\alpha,k}(x;\;-\beta)}{D(1-p)(\beta+\gamma)},&D>0,\\[9pt] \dfrac{\varphi_{\alpha,k}(x)+\gamma \Psi_{\alpha,k}(x;\;\gamma)}{c(1-p)},&D=0, \end{cases}\end{align*}

and

\begin{align}\Psi_{\alpha,k}(x;\;b)\;:\!=\; \int_{0}^x {\mathrm{e}}^{b(x-z)}\varphi_{\alpha,k}(z)\,\mathrm{d} z,\quad b \in \mathbb{R}. \end{align}

\begin{align}\Psi_{\alpha,k}(x;\;b)\;:\!=\; \int_{0}^x {\mathrm{e}}^{b(x-z)}\varphi_{\alpha,k}(z)\,\mathrm{d} z,\quad b \in \mathbb{R}. \end{align}

Remark 2.2. There is an alternative version of the q-scale function

$Z^{(q)}\colon \mathbb{R} \to [1,\infty)$

, defined as

$Z^{(q)}\colon \mathbb{R} \to [1,\infty)$

, defined as

\begin{align*}Z^{(q)}(x) = 1 + q\int_0^x W^{(q)}(z)\,\mathrm{d} z, \quad x\in \mathbb{R},\end{align*}

\begin{align*}Z^{(q)}(x) = 1 + q\int_0^x W^{(q)}(z)\,\mathrm{d} z, \quad x\in \mathbb{R},\end{align*}

where we regard that

$\int_0^x = 0$

if

$\int_0^x = 0$

if

$x<0$

. Note that

$x<0$

. Note that

$W^{(q)}(x) = q^{-1} \partial_x Z^{(q)}(x)$

as

$W^{(q)}(x) = q^{-1} \partial_x Z^{(q)}(x)$

as

$q\ne 0$

. The Laguerre-type expansion of

$q\ne 0$

. The Laguerre-type expansion of

$Z^{(q)}$

is also defined as

$Z^{(q)}$

is also defined as

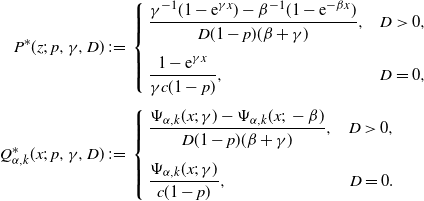

\begin{align}Z^{(q)}_K(x) &= 1 + q \int_0^x W^{(q)}_K(z)\,\mathrm{d} z \notag\\[5pt] &= 1 + q\bigl[ P^*(x;\; p,\gamma,D) - {\boldsymbol{Q}}^*_{\alpha,K}(x;\;p,\gamma,D)\cdot \boldsymbol{a}^G_{\alpha,K}\bigr], \end{align}

\begin{align}Z^{(q)}_K(x) &= 1 + q \int_0^x W^{(q)}_K(z)\,\mathrm{d} z \notag\\[5pt] &= 1 + q\bigl[ P^*(x;\; p,\gamma,D) - {\boldsymbol{Q}}^*_{\alpha,K}(x;\;p,\gamma,D)\cdot \boldsymbol{a}^G_{\alpha,K}\bigr], \end{align}

where

${\boldsymbol{Q}}^*_{\alpha,K}\;:\!=\; \bigl(Q^*_{\alpha,0}, Q^*_{\alpha,1},\ldots, Q^*_{\alpha,K}\bigr)^\top$

with

${\boldsymbol{Q}}^*_{\alpha,K}\;:\!=\; \bigl(Q^*_{\alpha,0}, Q^*_{\alpha,1},\ldots, Q^*_{\alpha,K}\bigr)^\top$

with

\begin{align*}P^*(z;\;p,\gamma,D)&\;:\!=\; \left\{ \begin{aligned} &\dfrac{\gamma^{-1}(1 - {\mathrm{e}}^{\gamma x})-\beta^{-1}(1-{\mathrm{e}}^{-\beta x})}{D(1-p)(\beta+\gamma)},&D>0,\\[5pt] &\dfrac{1 - {\mathrm{e}}^{\gamma x}}{\gamma c(1-p)},&D=0, \end{aligned}\right. \\[5pt] Q^*_{\alpha,k}(x;\;p,\gamma,D)&\;:\!=\; \left\{ \begin{aligned} &\dfrac{\Psi_{\alpha,k}(x;\;\gamma) - \Psi_{\alpha,k}(x;\;-\beta)}{D(1-p)(\beta+\gamma)},&D>0,\\[5pt] &\dfrac{\Psi_{\alpha,k}(x;\;\gamma)}{c(1-p)},&D=0. \end{aligned}\right.\end{align*}

\begin{align*}P^*(z;\;p,\gamma,D)&\;:\!=\; \left\{ \begin{aligned} &\dfrac{\gamma^{-1}(1 - {\mathrm{e}}^{\gamma x})-\beta^{-1}(1-{\mathrm{e}}^{-\beta x})}{D(1-p)(\beta+\gamma)},&D>0,\\[5pt] &\dfrac{1 - {\mathrm{e}}^{\gamma x}}{\gamma c(1-p)},&D=0, \end{aligned}\right. \\[5pt] Q^*_{\alpha,k}(x;\;p,\gamma,D)&\;:\!=\; \left\{ \begin{aligned} &\dfrac{\Psi_{\alpha,k}(x;\;\gamma) - \Psi_{\alpha,k}(x;\;-\beta)}{D(1-p)(\beta+\gamma)},&D>0,\\[5pt] &\dfrac{\Psi_{\alpha,k}(x;\;\gamma)}{c(1-p)},&D=0. \end{aligned}\right.\end{align*}

According to Lemma 2.3, if

$\overline{G}_q \in \mathcal{W}_\alpha^r(\mathbb{R}_+)$

(e.g.

$\overline{G}_q \in \mathcal{W}_\alpha^r(\mathbb{R}_+)$

(e.g.

$f\;:\!=\; \overline{G}_q$

satisfies (2.3)), then

$f\;:\!=\; \overline{G}_q$

satisfies (2.3)), then

\begin{align*}\sup_{x\in \mathbb{R}_+}|W^{(q)}_K(x) - W^{(q)}(x)| \to 0,\quad K\to \infty;\end{align*}

\begin{align*}\sup_{x\in \mathbb{R}_+}|W^{(q)}_K(x) - W^{(q)}(x)| \to 0,\quad K\to \infty;\end{align*}

see (2.7). Therefore it follows for any compact sets

$V\subset \mathbb{R}_+$

that

$V\subset \mathbb{R}_+$

that

\begin{align*}\sup_{x\in V}|Z^{(q)}_K(x) - Z^{(q)}(x)| \to 0,\quad K\to \infty.\end{align*}

\begin{align*}\sup_{x\in V}|Z^{(q)}_K(x) - Z^{(q)}(x)| \to 0,\quad K\to \infty.\end{align*}

Remark 2.3. The approximation formulas obtained in equations (2.9) and (2.11) are fundamentally different from those in Xie et al. [Reference Xie, Cui and Zhang27], while being more elementary. Their approximation focuses on the relationship between the probability density of the ‘killed process’

$X_{e_t}$

(where

$X_{e_t}$

(where

$e_t$

is an exponential random variable with mean 1) and its scale function, cleverly expanding the probability density into a Laguerre series. In our approximation, we utilize a Laguerre series expansion for the compound geometric distribution

$e_t$

is an exponential random variable with mean 1) and its scale function, cleverly expanding the probability density into a Laguerre series. In our approximation, we utilize a Laguerre series expansion for the compound geometric distribution

$\overline{G}_q$

, which is essentially similar to the approach of Shimizu and Zhang [Reference Shimizu and Zhimin24]. The utility of this approach becomes apparent in the subsequent discussion.

$\overline{G}_q$

, which is essentially similar to the approach of Shimizu and Zhang [Reference Shimizu and Zhimin24]. The utility of this approach becomes apparent in the subsequent discussion.

3. Statistical inference: main theorems

We will proceed with the statistical estimation of scale functions. When considering the practical application of q-scale functions, we typically focus on actuarial science, where

$X=(X_t)_{t\ge 0}$

represents the dynamics of an insurance surplus model. In this context, the coefficient of the linear term, c, corresponds to the premium rate. Therefore, in this paper, we specifically treat the value of c as known.

$X=(X_t)_{t\ge 0}$

represents the dynamics of an insurance surplus model. In this context, the coefficient of the linear term, c, corresponds to the premium rate. Therefore, in this paper, we specifically treat the value of c as known.

3.1. Sampling scheme

Let

$n\in \mathbb{N}$

. We assume that the process

$n\in \mathbb{N}$

. We assume that the process

$X=(X_t)_{t\ge 0}$

is observed at discrete time points

$X=(X_t)_{t\ge 0}$

is observed at discrete time points

$t_i^n\;:\!=\; i\Delta_n\ (i=0,1,\ldots,n)$

for some number

$t_i^n\;:\!=\; i\Delta_n\ (i=0,1,\ldots,n)$

for some number

$\Delta_n>0$

:

$\Delta_n>0$

:

\begin{align*}{\boldsymbol{X}}^n\;:\!=\; \{X_{t_i^n} \mid i = 0,1,\ldots, n\}, \quad T_n\;:\!=\; n\Delta_n.\end{align*}

\begin{align*}{\boldsymbol{X}}^n\;:\!=\; \{X_{t_i^n} \mid i = 0,1,\ldots, n\}, \quad T_n\;:\!=\; n\Delta_n.\end{align*}

In particular, the initial value

$X_{t_0^n} = x$

is assumed to be known. Moreover, we assume that ‘large’ jumps of X are observed. That is, for some number

$X_{t_0^n} = x$

is assumed to be known. Moreover, we assume that ‘large’ jumps of X are observed. That is, for some number

${\epsilon}_n>0$

, we can identify the jumps whose sizes are larger than

${\epsilon}_n>0$

, we can identify the jumps whose sizes are larger than

${\epsilon}_n$

, which are finitely many on

${\epsilon}_n$

, which are finitely many on

$[0,T_n]$

:

$[0,T_n]$

:

\begin{align*}{\boldsymbol{J}}^n\;:\!=\; \{\Delta X_t\;:\!=\; X_t - X_{t-} \mid t\in [0,T_n],\ |\Delta X_t| > {\epsilon}_n \}.\end{align*}

\begin{align*}{\boldsymbol{J}}^n\;:\!=\; \{\Delta X_t\;:\!=\; X_t - X_{t-} \mid t\in [0,T_n],\ |\Delta X_t| > {\epsilon}_n \}.\end{align*}

Assume that we have data

${\boldsymbol{X}}^n \cup {\boldsymbol{J}}^n$

, and consider the following asymptotics:

${\boldsymbol{X}}^n \cup {\boldsymbol{J}}^n$

, and consider the following asymptotics:

\begin{align}\Delta_n\to 0,\quad T_n\to \infty,\quad {\epsilon}_n\to 0, \end{align}

\begin{align}\Delta_n\to 0,\quad T_n\to \infty,\quad {\epsilon}_n\to 0, \end{align}

as

$n\to \infty$

. We shall always use the limit

$n\to \infty$

. We shall always use the limit

$n\to \infty$

when considering the asymptotic symbols, and assume (3.1) for the sampling scheme

$n\to \infty$

when considering the asymptotic symbols, and assume (3.1) for the sampling scheme

$(\Delta_n,T_n,{\epsilon}_n)$

without further comment.

$(\Delta_n,T_n,{\epsilon}_n)$

without further comment.

Remark 3.1. The data

${\boldsymbol{X}}^n$

are assumed to represent the data on the remaining reserves that insurance companies record on a regular basis. On the other hand,

${\boldsymbol{X}}^n$

are assumed to represent the data on the remaining reserves that insurance companies record on a regular basis. On the other hand,

${\boldsymbol{J}}^n$

are assumed to be ‘large’ claims. It may seem unnatural to consider such a model with infinitely many jumps when modeling insurance surplus, but this is a standard surplus approximation in risk theory. Arguing under asymptotics such as (3.1) with data like

${\boldsymbol{J}}^n$

are assumed to be ‘large’ claims. It may seem unnatural to consider such a model with infinitely many jumps when modeling insurance surplus, but this is a standard surplus approximation in risk theory. Arguing under asymptotics such as (3.1) with data like

${\boldsymbol{J}}^n$

is a common way of theoretically justifying that the more detailed claims data you collect, the better the estimation. In practice, it is not necessary to observe infinitely many ‘small’ jumps.

${\boldsymbol{J}}^n$

is a common way of theoretically justifying that the more detailed claims data you collect, the better the estimation. In practice, it is not necessary to observe infinitely many ‘small’ jumps.

We shall make some assumptions on the scheme

$(\Delta_n,T_n,{\epsilon}_n)$

:

$(\Delta_n,T_n,{\epsilon}_n)$

:

S1

$n\Delta_n^2\to 0$

,

$n\Delta_n^2\to 0$

,

S2

$\displaystyle \int_0^{{\epsilon}_n} z\,\nu(\mathrm{d} z) + \int_0^{{\epsilon}_n} z^2\,\nu(\mathrm{d} z) = {\mathrm{o}} \bigl(T_n^{-1/2}\bigr)$

.

$\displaystyle \int_0^{{\epsilon}_n} z\,\nu(\mathrm{d} z) + \int_0^{{\epsilon}_n} z^2\,\nu(\mathrm{d} z) = {\mathrm{o}} \bigl(T_n^{-1/2}\bigr)$

.

In addition, to ensure some integrability with respect to

$\nu$

, we will prepare the following moment conditions on

$\nu$

, we will prepare the following moment conditions on

$\nu$

:

$\nu$

:

M[

k

] For some given

$k>0$

, there exists some

$k>0$

, there exists some

${\epsilon}\in (0,1)$

such that

${\epsilon}\in (0,1)$

such that

$\nu( |z|\vee |z|^{k + {\epsilon}}) < \infty$

.

$\nu( |z|\vee |z|^{k + {\epsilon}}) < \infty$

.

3.2. Main theorems

For the statistical argument, we let

$p_0, D_0$

, and

$p_0, D_0$

, and

$\gamma_0$

denote the true values of parameters p, D, and

$\gamma_0$

denote the true values of parameters p, D, and

$\gamma$

, respectively. We will provide estimators for approximations

$\gamma$

, respectively. We will provide estimators for approximations

$W_K^{(q)}$

and

$W_K^{(q)}$

and

$Z_K^{(q)}$

, in which the parameters p, D, and

$Z_K^{(q)}$

, in which the parameters p, D, and

$\gamma$

are replaced by their true value.

$\gamma$

are replaced by their true value.

According to the expressions (2.9) and (2.11), we construct estimators of

$W_K^{(q)}$

and

$W_K^{(q)}$

and

$Z_K^{(q)}$

as follows:

$Z_K^{(q)}$

as follows:

\begin{align*}\widehat{W}^{(q)}_{K}(x)&\;:\!=\; P(x;\;\widehat{p}_{n},\widehat{\gamma}_{n},\widehat{D}_{n}) -{\boldsymbol{Q}}_{\alpha,K}(x;\;\widehat{p}_{n},\widehat{\gamma}_{n},\widehat{D}_{n})\cdot \widehat{\boldsymbol{a}}^{G}_{\alpha,K}, \\[5pt] \widehat{Z}^{(q)}_{K}(x)&\;:\!=\; q \bigl[P^*(x;\;\widehat{p}_{n},\widehat{\gamma}_{n},\widehat{D}_{n}) -{\boldsymbol{Q}}^*_{\alpha,K}(x;\;\widehat{p}_{n},\widehat{\gamma}_{n},\widehat{D}_{n})\cdot \widehat{\boldsymbol{a}}^{G}_{\alpha,K}\bigr].\end{align*}

\begin{align*}\widehat{W}^{(q)}_{K}(x)&\;:\!=\; P(x;\;\widehat{p}_{n},\widehat{\gamma}_{n},\widehat{D}_{n}) -{\boldsymbol{Q}}_{\alpha,K}(x;\;\widehat{p}_{n},\widehat{\gamma}_{n},\widehat{D}_{n})\cdot \widehat{\boldsymbol{a}}^{G}_{\alpha,K}, \\[5pt] \widehat{Z}^{(q)}_{K}(x)&\;:\!=\; q \bigl[P^*(x;\;\widehat{p}_{n},\widehat{\gamma}_{n},\widehat{D}_{n}) -{\boldsymbol{Q}}^*_{\alpha,K}(x;\;\widehat{p}_{n},\widehat{\gamma}_{n},\widehat{D}_{n})\cdot \widehat{\boldsymbol{a}}^{G}_{\alpha,K}\bigr].\end{align*}

The consistency and asymptotic normality for

$\widehat{W}^{(q)}_K$

are obtained for each

$\widehat{W}^{(q)}_K$

are obtained for each

$K\in \mathbb{N}$

as follows.

$K\in \mathbb{N}$

as follows.

Theorem 3.1. Suppose the assumptions NPC, S1, S2, and M[2] hold. Then, for any

$q>0$

,

$q>0$

,

$K\in \mathbb{N}$

, and

$K\in \mathbb{N}$

, and

$x \in \mathbb{R}_+$

, we have

$x \in \mathbb{R}_+$

, we have

\begin{align*}\widehat{W}^{(q)}_K(x) \stackrel{p}{\to} W^{(q)}_K(x).\end{align*}

\begin{align*}\widehat{W}^{(q)}_K(x) \stackrel{p}{\to} W^{(q)}_K(x).\end{align*}

In particular, when

$q=0$

, we have uniform consistency:

$q=0$

, we have uniform consistency:

\begin{align*}\sup_{x\in\mathbb{R}_+}\bigl|\widehat{W}^{(0)}_K(x)-W^{(0)}_K(x)\bigr|\stackrel{p}{\to} 0.\end{align*}

\begin{align*}\sup_{x\in\mathbb{R}_+}\bigl|\widehat{W}^{(0)}_K(x)-W^{(0)}_K(x)\bigr|\stackrel{p}{\to} 0.\end{align*}

In addition, suppose M[4] holds. Then we have

\begin{align*}\sqrt{T_{n}}\bigl(\widehat{W}^{(q)}_{K}(x)-W^{(q)}_{K}(x)\bigr)\stackrel{d}{\to} N (0,\sigma_{K}(x)),\end{align*}

\begin{align*}\sqrt{T_{n}}\bigl(\widehat{W}^{(q)}_{K}(x)-W^{(q)}_{K}(x)\bigr)\stackrel{d}{\to} N (0,\sigma_{K}(x)),\end{align*}

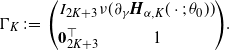

where

$\sigma_{K}(x)\;:\!=\; [C_{K}(x)\Gamma_{K}]\Sigma_{K}[C_{K}(x)\Gamma_{K}]^{\top}$

with

$\sigma_{K}(x)\;:\!=\; [C_{K}(x)\Gamma_{K}]\Sigma_{K}[C_{K}(x)\Gamma_{K}]^{\top}$

with

$\Sigma_{K}$

and

$\Sigma_{K}$

and

$\Gamma_{K}$

given in (B.1) and (B.2), respectively, and

$\Gamma_{K}$

given in (B.1) and (B.2), respectively, and

$C_K$

is the

$C_K$

is the

$(2K+4)$

-dim vector given by

$(2K+4)$

-dim vector given by

\begin{align*}&C_{K}(x)\;:\!=\; \\[5pt] &\ \bigl({\boldsymbol{Q}}_{\alpha,K}(x;\;p_0,\gamma_0,D_0)^\top \bigl(A_K^f\bigr)^{-1}B_{K},\partial_{(p,\gamma)}\bigl[P(x;\;\gamma_0,p_0,D_0)-{\boldsymbol{Q}}_{\alpha,K}(x;\;p_0,\gamma_0,D_0)\cdot \boldsymbol{a}^{G}_{\alpha,K}\bigr]\bigr)^\top ,\end{align*}

\begin{align*}&C_{K}(x)\;:\!=\; \\[5pt] &\ \bigl({\boldsymbol{Q}}_{\alpha,K}(x;\;p_0,\gamma_0,D_0)^\top \bigl(A_K^f\bigr)^{-1}B_{K},\partial_{(p,\gamma)}\bigl[P(x;\;\gamma_0,p_0,D_0)-{\boldsymbol{Q}}_{\alpha,K}(x;\;p_0,\gamma_0,D_0)\cdot \boldsymbol{a}^{G}_{\alpha,K}\bigr]\bigr)^\top ,\end{align*}

with the matrix

$B_K$

given in Corollary B.1.

$B_K$

given in Corollary B.1.

Proof. See Section C.6.

Theorem 3.2. Suppose the assumptions NPC, S1, S2, and M[2] hold. Then, for any

$q>0$

,

$q>0$

,

$K\in \mathbb{N}$

, and

$K\in \mathbb{N}$

, and

$x \in \mathbb{R}_+$

, we have

$x \in \mathbb{R}_+$

, we have

\begin{align*}\widehat{Z}^{(q)}_K(x) \stackrel{p}{\to} Z^{(q)}_K(x).\end{align*}

\begin{align*}\widehat{Z}^{(q)}_K(x) \stackrel{p}{\to} Z^{(q)}_K(x).\end{align*}

In particular, when

$q=0$

, we have uniform consistency: for any compact set

$q=0$

, we have uniform consistency: for any compact set

$V\subset \mathbb{R}_+$

,

$V\subset \mathbb{R}_+$

,

\begin{align*}\sup_{x\in V}\bigl|\widehat{Z}^{(0)}_K(x)-Z^{(0)}_K(x)\bigr|\stackrel{p}{\to} 0.\end{align*}

\begin{align*}\sup_{x\in V}\bigl|\widehat{Z}^{(0)}_K(x)-Z^{(0)}_K(x)\bigr|\stackrel{p}{\to} 0.\end{align*}

In addition, suppose M[4] holds. Then we have

\begin{align*}\sqrt{T_{n}}\bigl(\widehat{Z}^{(q)}_K(x)-Z^{(q)}_K(x)\bigr)\stackrel{d}{\to} N\bigl(0,\sigma^*_{K}(x)\bigr),\end{align*}

\begin{align*}\sqrt{T_{n}}\bigl(\widehat{Z}^{(q)}_K(x)-Z^{(q)}_K(x)\bigr)\stackrel{d}{\to} N\bigl(0,\sigma^*_{K}(x)\bigr),\end{align*}

where

$\sigma^*_{K}(x)\;:\!=\; q^2[C^*_K(x)\Gamma_K]\Sigma_K[C^*_K(x)\Gamma_K]^\top$

with

$\sigma^*_{K}(x)\;:\!=\; q^2[C^*_K(x)\Gamma_K]\Sigma_K[C^*_K(x)\Gamma_K]^\top$

with

$\Sigma_K$

and

$\Sigma_K$

and

$\Gamma_K$

given in (B.1) and (B.2), respectively, and

$\Gamma_K$

given in (B.1) and (B.2), respectively, and

$C^*_K$

is the

$C^*_K$

is the

$(2K+4)$

-dim vector given by

$(2K+4)$

-dim vector given by

\begin{align*}&C^*_K(x)\;:\!=\; \\[5pt] &\ \bigl({\boldsymbol{Q}}^*_{\alpha,K}(x;\;p_0,\gamma_0,D_0)^\top\bigl(A_K^f\bigr)^{-1}B_{K},\partial_{(p,\gamma)}\bigl[P^*(x;\;\gamma_0,p_0,D_0)-{\boldsymbol{Q}}^*_{\alpha,K}(x;\;p_0,\gamma_0,D_0)\cdot \boldsymbol{a}^{G}_{\alpha,K}\bigr]\bigr)^\top ,\end{align*}

\begin{align*}&C^*_K(x)\;:\!=\; \\[5pt] &\ \bigl({\boldsymbol{Q}}^*_{\alpha,K}(x;\;p_0,\gamma_0,D_0)^\top\bigl(A_K^f\bigr)^{-1}B_{K},\partial_{(p,\gamma)}\bigl[P^*(x;\;\gamma_0,p_0,D_0)-{\boldsymbol{Q}}^*_{\alpha,K}(x;\;p_0,\gamma_0,D_0)\cdot \boldsymbol{a}^{G}_{\alpha,K}\bigr]\bigr)^\top ,\end{align*}

with the matrix

$B_K$

given in Corollary B.1.

$B_K$

given in Corollary B.1.

Proof. See Section C.7.

Corollary 3.1. Suppose the assumptions NPC, S1, S2, and M[2] hold. Then, for any

$q>0$

,

$q>0$

,

$K\in \mathbb{N}$

, and

$K\in \mathbb{N}$

, and

$x \in \mathbb{R}_+$

, we have

$x \in \mathbb{R}_+$

, we have

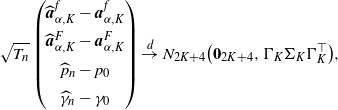

\begin{align*}\sqrt{T_{n}} \begin{pmatrix} \widehat{W}^{(q)}_{K}(x)-W^{(q)}_{K}(x)\\[5pt] \widehat{Z}^{(q)}_{K}(x)-Z^{(q)}_{K}(x) \end{pmatrix}\stackrel{d}{\to} N_{2}\bigl(\boldsymbol{0}_{2},\widetilde{\Sigma}_{K}(x)\bigr),\end{align*}

\begin{align*}\sqrt{T_{n}} \begin{pmatrix} \widehat{W}^{(q)}_{K}(x)-W^{(q)}_{K}(x)\\[5pt] \widehat{Z}^{(q)}_{K}(x)-Z^{(q)}_{K}(x) \end{pmatrix}\stackrel{d}{\to} N_{2}\bigl(\boldsymbol{0}_{2},\widetilde{\Sigma}_{K}(x)\bigr),\end{align*}

where

\begin{align*}\widetilde{\Sigma}_{K}(x)\;:\!=\; \biggl[ \begin{pmatrix} C_{K}(x)\\[5pt] qC^{*}_{K}(x) \end{pmatrix}\Gamma_{K}\biggr]\Sigma_{K}\biggl[ \begin{pmatrix} C_{K}(x)\\[5pt] qC^{*}_{K}(x) \end{pmatrix}\Gamma_{K}\biggr]^{\top}.\end{align*}

\begin{align*}\widetilde{\Sigma}_{K}(x)\;:\!=\; \biggl[ \begin{pmatrix} C_{K}(x)\\[5pt] qC^{*}_{K}(x) \end{pmatrix}\Gamma_{K}\biggr]\Sigma_{K}\biggl[ \begin{pmatrix} C_{K}(x)\\[5pt] qC^{*}_{K}(x) \end{pmatrix}\Gamma_{K}\biggr]^{\top}.\end{align*}

Proof. See Section C.8.

Remark 3.2. Our asymptotic results for

$\widehat{W}_K^{(q)}$

and

$\widehat{W}_K^{(q)}$

and

$\widehat{Z}_K^{(q)}$

are all for a fixed

$\widehat{Z}_K^{(q)}$

are all for a fixed

$K\in \mathbb{N}$

, and but one may also be concerned with the case where

$K\in \mathbb{N}$

, and but one may also be concerned with the case where

$K=K_n\to \infty$

as well as

$K=K_n\to \infty$

as well as

$n\to \infty$

. It is not a straightforward extension, even for consistency. For example, if we could show that for each

$n\to \infty$

. It is not a straightforward extension, even for consistency. For example, if we could show that for each

$x\in \mathbb{R}_+$

,

$x\in \mathbb{R}_+$

,

\begin{align*}\sup_{K\in \mathbb{N}}\bigl|\widehat{W}_K^{(q)}(x) - W_K^{(q)}(x)\bigr| \stackrel{p}{\to} 0,\quad n\to \infty,\end{align*}

\begin{align*}\sup_{K\in \mathbb{N}}\bigl|\widehat{W}_K^{(q)}(x) - W_K^{(q)}(x)\bigr| \stackrel{p}{\to} 0,\quad n\to \infty,\end{align*}

then we can exchange the order of the limits

$n\to \infty$

and

$n\to \infty$

and

$K\to \infty$

, which concludes that

$K\to \infty$

, which concludes that

$\widehat{W}_\infty^{(q)}(x) \stackrel{p}{\to} W_\infty^{(q)}(x)$

for each

$\widehat{W}_\infty^{(q)}(x) \stackrel{p}{\to} W_\infty^{(q)}(x)$

for each

$x\in \mathbb{R}_+$

. On this point, we need further study. As for the extension of asymptotic normality, a more complicated discussion is needed to extend the results to the case where K depends on n with

$x\in \mathbb{R}_+$

. On this point, we need further study. As for the extension of asymptotic normality, a more complicated discussion is needed to extend the results to the case where K depends on n with

$K=K_n\to \infty$

. This will lead to a high-dimensional setting, and we will need a high-dimensional central limit theorem (CLT) for triangular arrays, even without a martingale property. A sophisticated CLT would still need to be proved.

$K=K_n\to \infty$

. This will lead to a high-dimensional setting, and we will need a high-dimensional central limit theorem (CLT) for triangular arrays, even without a martingale property. A sophisticated CLT would still need to be proved.

Appendix A. Some auxiliary statistics

A.1. Estimator of

$\boldsymbol{D}_{\textbf{0}}$

For

$D=\sigma^2/2$

, we consider the following estimator proposed by Jacod [Reference Jacod12] and Shimizu [Reference Shimizu22, Reference Shimizu23]: for each fixed

$D=\sigma^2/2$

, we consider the following estimator proposed by Jacod [Reference Jacod12] and Shimizu [Reference Shimizu22, Reference Shimizu23]: for each fixed

$T>0$

,

$T>0$

,

\begin{align*}\widehat{D}^{T}_{n}\;:\!=\; \dfrac{1}{2T}\Biggl(\sum_{i=1}^{\lfloor T\Delta_{n}^{-1}\rfloor}|X_{i\Delta_{n}}-X_{(i-1)\Delta_{n}}|^{2}-\sum_{s\le T}|\Delta L_{s}|^{2}\boldsymbol{1}_{\{\Delta L_{s}>{\epsilon}_n\}}\Biggr).\end{align*}

\begin{align*}\widehat{D}^{T}_{n}\;:\!=\; \dfrac{1}{2T}\Biggl(\sum_{i=1}^{\lfloor T\Delta_{n}^{-1}\rfloor}|X_{i\Delta_{n}}-X_{(i-1)\Delta_{n}}|^{2}-\sum_{s\le T}|\Delta L_{s}|^{2}\boldsymbol{1}_{\{\Delta L_{s}>{\epsilon}_n\}}\Biggr).\end{align*}

Lemma A.1. (Shimizu [Reference Shimizu22], Remark 3.2.) Under the assumptions S1 and S2, the estimator

$\widehat{D}^T_n$

is consistent with

$\widehat{D}^T_n$

is consistent with

$D_0$

with the rate of convergence being faster than

$D_0$

with the rate of convergence being faster than

$\sqrt{T_n}$

such that for any

$\sqrt{T_n}$

such that for any

$t>0$

,

$t>0$

,

\begin{align*}\sqrt{T_n}\bigl(\widehat{D}^T_n - D_0\bigr) \stackrel{p}{\to} 0.\end{align*}

\begin{align*}\sqrt{T_n}\bigl(\widehat{D}^T_n - D_0\bigr) \stackrel{p}{\to} 0.\end{align*}

Remark A.1. Since the constant

$T>0$

in the estimator

$T>0$

in the estimator

$\widehat{D}^T_n$

can be arbitrary, we will fix it to be

$\widehat{D}^T_n$

can be arbitrary, we will fix it to be

$T=1$

without loss of generality, and set

$T=1$

without loss of generality, and set

\begin{align*}\widehat{D}_n \;:\!=\; \widehat{D}_n^1.\end{align*}

\begin{align*}\widehat{D}_n \;:\!=\; \widehat{D}_n^1.\end{align*}

In practice, the value of T should be chosen appropriately based on the amount of data and the size of

$\Delta_n$

.

$\Delta_n$

.

A.2. Estimator of

$\nu$

-functionals

First, we would like to estimate the integral-type functional

$\nu (\boldsymbol{H}_\theta)$

, where

$\nu (\boldsymbol{H}_\theta)$

, where

$\boldsymbol{H}_\theta\colon \mathbb{R}_+\to \mathbb{R}^d$

is a

$\boldsymbol{H}_\theta\colon \mathbb{R}_+\to \mathbb{R}^d$

is a

$\nu$

-integrable function with an unknown parameter

$\nu$

-integrable function with an unknown parameter

$\theta\in \Theta$

:

$\theta\in \Theta$

:

\begin{align*}\nu(\boldsymbol{H}_\theta) \;:\!=\; \biggl( \int_0^\infty H_\theta^{(1)}(z)\,\nu(\mathrm{d} z), \ldots, \int_0^\infty H_\theta^{(d)}(z)\,\nu(\mathrm{d} z)\biggr),\end{align*}

\begin{align*}\nu(\boldsymbol{H}_\theta) \;:\!=\; \biggl( \int_0^\infty H_\theta^{(1)}(z)\,\nu(\mathrm{d} z), \ldots, \int_0^\infty H_\theta^{(d)}(z)\,\nu(\mathrm{d} z)\biggr),\end{align*}

where

$\Theta$

is an open and bounded subset of

$\Theta$

is an open and bounded subset of

$\mathbb{R}^l$

for some

$\mathbb{R}^l$

for some

$l\in \mathbb{N}$

. Note that the parameter

$l\in \mathbb{N}$

. Note that the parameter

$\theta$

can be a variety of parameters depending on the context. For instance, we will see later that the parameter

$\theta$

can be a variety of parameters depending on the context. For instance, we will see later that the parameter

$p\;:\!=\; \int_0^\infty \widetilde{f}_q(z)\,\mathrm{d} z$

, the coefficients of Laguerre expansion, e.g.

$p\;:\!=\; \int_0^\infty \widetilde{f}_q(z)\,\mathrm{d} z$

, the coefficients of Laguerre expansion, e.g.

$a_{\alpha,k}^f$

and

$a_{\alpha,k}^f$

and

$a_{\alpha,k}^F$

, can all be expressed in terms of the integral functional of

$a_{\alpha,k}^F$

, can all be expressed in terms of the integral functional of

$\nu$

.

$\nu$

.

In short, we need to estimate the parameters

$(D_0,\gamma_0, \nu(\boldsymbol{H}_{\theta_0}))$

, where

$(D_0,\gamma_0, \nu(\boldsymbol{H}_{\theta_0}))$

, where

$\theta_0$

is the true value of

$\theta_0$

is the true value of

$\theta$

. Hereafter, we assume that there exists an open and bounded set

$\theta$

. Hereafter, we assume that there exists an open and bounded set

$\Theta_1$

and

$\Theta_1$

and

$\Theta_2$

of

$\Theta_2$

of

$\mathbb{R}_+$

such that

$\mathbb{R}_+$

such that

\begin{align*}(D_0,\gamma_0,\theta_0)\in \Theta_1\times \Theta_2.\end{align*}

\begin{align*}(D_0,\gamma_0,\theta_0)\in \Theta_1\times \Theta_2.\end{align*}

Moreover, we make the following assumptions on an integrands

$\boldsymbol{H}_\theta$

, which are applied to a variety of

$\boldsymbol{H}_\theta$

, which are applied to a variety of

$\boldsymbol{H}_\theta$

, locally in this section.

$\boldsymbol{H}_\theta$

, locally in this section.

H1[

$\delta$

] For each

$\delta$

] For each

$\theta\in \Theta$

, there exists a

$\theta\in \Theta$

, there exists a

$\delta\ge 0$

such that

$\delta\ge 0$

such that

$\nu(|\boldsymbol{H}_\theta| \vee|\boldsymbol{H}_\theta|^{2+\delta}) < \infty$

.

$\nu(|\boldsymbol{H}_\theta| \vee|\boldsymbol{H}_\theta|^{2+\delta}) < \infty$

.

H2

$\displaystyle \sup_{\theta \in \overline{\Theta}} \nu(|\boldsymbol{H}_\theta| \vee |\boldsymbol{H}_\theta|^2) < \infty$

.

$\displaystyle \sup_{\theta \in \overline{\Theta}} \nu(|\boldsymbol{H}_\theta| \vee |\boldsymbol{H}_\theta|^2) < \infty$

.

H3 There exists a

$\nu$

-integrable function

$\nu$

-integrable function

$h_1\colon \mathbb{R}_+\to \mathbb{R}$

such that

$h_1\colon \mathbb{R}_+\to \mathbb{R}$

such that

\begin{align*}\sup_{\theta \in \overline{\Theta}} |\boldsymbol{H}_\theta(z)| \le h_1(z).\end{align*}

\begin{align*}\sup_{\theta \in \overline{\Theta}} |\boldsymbol{H}_\theta(z)| \le h_1(z).\end{align*}

H4 There exists a function

$h_2\colon \mathbb{R}_+\to \mathbb{R}$

with

$h_2\colon \mathbb{R}_+\to \mathbb{R}$

with

$\nu\bigl(h_2\vee h_2^2\bigr) < \infty$

such that for any

$\nu\bigl(h_2\vee h_2^2\bigr) < \infty$

such that for any

$\kappa \in \mathbb{R}^l$

,

$\kappa \in \mathbb{R}^l$

,

\begin{align*}\sup_{\theta \in \overline{\Theta}} |\boldsymbol{H}_{\theta + \kappa}(z) - \boldsymbol{H}_\theta(z)| \le h_2(z)|\kappa|.\end{align*}

\begin{align*}\sup_{\theta \in \overline{\Theta}} |\boldsymbol{H}_{\theta + \kappa}(z) - \boldsymbol{H}_\theta(z)| \le h_2(z)|\kappa|.\end{align*}

H5 For each

$i=1,\ldots,d$

,

$i=1,\ldots,d$

,

\begin{align*}\int_0^{{\epsilon}_n} H_\theta^{(i)}(z)\,\nu(\mathrm{d} z) = {\mathrm{o}} \bigl(T_n^{-1/2}\bigr).\end{align*}

\begin{align*}\int_0^{{\epsilon}_n} H_\theta^{(i)}(z)\,\nu(\mathrm{d} z) = {\mathrm{o}} \bigl(T_n^{-1/2}\bigr).\end{align*}

As for functionals

$\nu(\boldsymbol{H}_\theta)$

, we can use the following threshold-type estimator:

$\nu(\boldsymbol{H}_\theta)$

, we can use the following threshold-type estimator:

\begin{align*}\widehat{\nu}_n(\boldsymbol{H}_\theta) \;:\!=\; \dfrac{1}{T_n} \sum_{t \in (0, T_n]} \boldsymbol{H}_\theta(\Delta L_t) \boldsymbol{1}_{\{\Delta L_t > {\epsilon}_n\}}.\end{align*}

\begin{align*}\widehat{\nu}_n(\boldsymbol{H}_\theta) \;:\!=\; \dfrac{1}{T_n} \sum_{t \in (0, T_n]} \boldsymbol{H}_\theta(\Delta L_t) \boldsymbol{1}_{\{\Delta L_t > {\epsilon}_n\}}.\end{align*}

Lemma A.2. (Shimizu [Reference Shimizu22], Propositions 3.1 and 3.2.)

-

(1) Under the assumption H1[0], we have

In addition, assuming further H2 and H4, we have uniform consistency:

\begin{align*}\widehat{\nu}_n(\boldsymbol{H}_\theta) \stackrel{p}{\to} \nu(\boldsymbol{H}_\theta),\quad \theta \in \Theta.\end{align*}

\begin{align*}\sup_{\theta \in \overline{\Theta}} |\widehat{\nu}_n(\boldsymbol{H}_\theta) - \nu(\boldsymbol{H}_\theta)| \to 0.\end{align*}

-

(2) Under H1[

$\delta$

] for some

$\delta>0$

and H5, we have where

\begin{align*}\sqrt{T_n}(\widehat{\nu}_n(\boldsymbol{H}_\theta) - \nu(\boldsymbol{H}_\theta)) \stackrel{d}{\to} N_d({\boldsymbol 0}_d,\Sigma_\theta), \quad \theta \in \Theta,\end{align*}

$\Sigma_\theta = \bigl(\nu\bigl(H_\theta^{(i)}H_\theta^{(j)}\bigr)\bigr)_{1\le i,j\le d}$

.

It will be easy to see that the following version of the continuous mapping-type theorem holds for the estimator

$\widehat{\nu}_n(\boldsymbol{H}_\theta)$

.

$\widehat{\nu}_n(\boldsymbol{H}_\theta)$

.

Corollary A.1. Under the assumptions H1[0], H2–H4, it follows that

\begin{align*}\widehat{\nu}_n\bigl(\boldsymbol{H}\boldsymbol{H}_{\widehat{\theta}_n}\bigr) \stackrel{p}{\to} \nu(\boldsymbol{H}_{\theta_0}),\end{align*}

\begin{align*}\widehat{\nu}_n\bigl(\boldsymbol{H}\boldsymbol{H}_{\widehat{\theta}_n}\bigr) \stackrel{p}{\to} \nu(\boldsymbol{H}_{\theta_0}),\end{align*}

for any random sequence such that

$\widehat{\theta}_n \stackrel{p}{\to} \theta_0\in \Theta$

.

$\widehat{\theta}_n \stackrel{p}{\to} \theta_0\in \Theta$

.

Proof. Note that there exists a sub-subsequence

$\{\widehat{\theta}_{n'}\}$

for any subsequence of

$\{\widehat{\theta}_{n'}\}$

for any subsequence of

$\{\widehat{\theta}_n\}$

such that

$\{\widehat{\theta}_n\}$

such that

$\widehat{\theta}_{n'} \to \theta_0$

a.s. Then, under the assumption H3, we can apply the Lebesgue-dominated convergence theorem to obtain

$\widehat{\theta}_{n'} \to \theta_0$

a.s. Then, under the assumption H3, we can apply the Lebesgue-dominated convergence theorem to obtain

$\nu\bigl(\boldsymbol{H}_{\widehat{\theta}_{n'}}\bigr)\to\nu(\boldsymbol{H}_{\theta_0})$

a.s. That is, the sequence

$\nu\bigl(\boldsymbol{H}_{\widehat{\theta}_{n'}}\bigr)\to\nu(\boldsymbol{H}_{\theta_0})$

a.s. That is, the sequence

$\bigl\{\nu\bigl(\boldsymbol{H}_{\widehat{\theta}_n}\bigr)\bigr\}$

has a sub-subsequence that converges to

$\bigl\{\nu\bigl(\boldsymbol{H}_{\widehat{\theta}_n}\bigr)\bigr\}$

has a sub-subsequence that converges to

$\nu(\boldsymbol{H}_{\theta_0})$

almost surely, which implies that

$\nu(\boldsymbol{H}_{\theta_0})$

almost surely, which implies that

$\nu\bigl(\boldsymbol{H}_{\widehat{\theta}_n}\bigr)\stackrel{p}{\to}\nu(\boldsymbol{H}_{\theta_0})$

. Moreover, since

$\nu\bigl(\boldsymbol{H}_{\widehat{\theta}_n}\bigr)\stackrel{p}{\to}\nu(\boldsymbol{H}_{\theta_0})$

. Moreover, since

${\mathbb{P}}(\widehat{\theta}_n\notin\Theta)\to 0$

, it follows from Lemma A.2 that for any

${\mathbb{P}}(\widehat{\theta}_n\notin\Theta)\to 0$

, it follows from Lemma A.2 that for any

${\epsilon}>0$

,

${\epsilon}>0$

,

\begin{align*}{\mathbb{P}}\bigl(|\widehat{\nu}_{n}\bigl(\boldsymbol{H}_{\widehat{\theta}_n}\bigr)-\nu(\boldsymbol{H}_{\theta_0})|>{\epsilon}\bigr)&\le {\mathbb{P}}\Bigl(\sup_{\theta\in \overline{\Theta}} |\widehat{\nu}_{n}(\boldsymbol{H}_\theta)-\nu(\boldsymbol{H}_\theta)|>{\epsilon}/2,\ \widehat{\theta}_n\in\Theta\Bigr)\\[5pt] &\quad +{\mathbb{P}}\bigl(|\nu\bigl(\boldsymbol{H}_{\widehat{\theta}_n}\bigr)-\nu(\boldsymbol{H}_{\theta_0})|>{\epsilon}/2,\ \widehat{\theta}_n\in\Theta\bigr) \\[5pt] &\quad + {\mathbb{P}}(\widehat{\theta}_n\notin\Theta) \to 0.\end{align*}

\begin{align*}{\mathbb{P}}\bigl(|\widehat{\nu}_{n}\bigl(\boldsymbol{H}_{\widehat{\theta}_n}\bigr)-\nu(\boldsymbol{H}_{\theta_0})|>{\epsilon}\bigr)&\le {\mathbb{P}}\Bigl(\sup_{\theta\in \overline{\Theta}} |\widehat{\nu}_{n}(\boldsymbol{H}_\theta)-\nu(\boldsymbol{H}_\theta)|>{\epsilon}/2,\ \widehat{\theta}_n\in\Theta\Bigr)\\[5pt] &\quad +{\mathbb{P}}\bigl(|\nu\bigl(\boldsymbol{H}_{\widehat{\theta}_n}\bigr)-\nu(\boldsymbol{H}_{\theta_0})|>{\epsilon}/2,\ \widehat{\theta}_n\in\Theta\bigr) \\[5pt] &\quad + {\mathbb{P}}(\widehat{\theta}_n\notin\Theta) \to 0.\end{align*}

This completes the proof.

A.3. Estimator of

$\gamma_0$

An estimator of the Lundberg exponent

$\gamma_0 = \Phi(q)$

is found in Shimizu [Reference Shimizu22] as an M-estimator given by

$\gamma_0 = \Phi(q)$

is found in Shimizu [Reference Shimizu22] as an M-estimator given by

\begin{align*}\widehat{\gamma}_n = \boldsymbol{1}_{\{q > 0\}}\cdot \arg\inf_{r \in \Theta_2}|c r + \widehat{D}_n r^2 - \widehat{\nu}_n(k_r) - q|^2,\end{align*}

\begin{align*}\widehat{\gamma}_n = \boldsymbol{1}_{\{q > 0\}}\cdot \arg\inf_{r \in \Theta_2}|c r + \widehat{D}_n r^2 - \widehat{\nu}_n(k_r) - q|^2,\end{align*}

where

$k_r(z) = {\mathrm{e}}^{-r z} - 1$

. This estimator is quite natural because the contrast function is a direct estimator of the Lundberg equation ‘

$k_r(z) = {\mathrm{e}}^{-r z} - 1$

. This estimator is quite natural because the contrast function is a direct estimator of the Lundberg equation ‘

$\psi_X(r) - q =0$

’, and it is useful because it satisfies consistency and asymptotic normality, as follows.

$\psi_X(r) - q =0$

’, and it is useful because it satisfies consistency and asymptotic normality, as follows.

Lemma A.3 (Shimizu [Reference Shimizu22], Lemma 3.3.) Suppose the conditions NPC, S1, S2, and M[2] hold. Then we have

\begin{align*}\sqrt{T_n}(\widehat{\gamma}_n - \gamma_0) \stackrel{d}{\to} N_1\bigl(0,v_0^2\bigr),\end{align*}

\begin{align*}\sqrt{T_n}(\widehat{\gamma}_n - \gamma_0) \stackrel{d}{\to} N_1\bigl(0,v_0^2\bigr),\end{align*}

where

\begin{align*}v_0^2 = \dfrac{\nu\bigl(k_{\gamma_0}^2\bigr)}{ (c + 2D_0\gamma_0 + \nu(\partial_r k_{\gamma_0}))^2}.\end{align*}

\begin{align*}v_0^2 = \dfrac{\nu\bigl(k_{\gamma_0}^2\bigr)}{ (c + 2D_0\gamma_0 + \nu(\partial_r k_{\gamma_0}))^2}.\end{align*}

In particular, we have the representation (in the proof of Lemma 3.3 of [Reference Shimizu22]) that

\begin{align}\sqrt{T_n}(\widehat{\gamma}_n - \gamma_0) = \sqrt{T_n}(\widehat{\nu}_n(\widetilde{H}_{\gamma_0}) - \nu(\widetilde{H}_{\gamma_0})) + {\mathrm{o}}_p(1), \end{align}

\begin{align}\sqrt{T_n}(\widehat{\gamma}_n - \gamma_0) = \sqrt{T_n}(\widehat{\nu}_n(\widetilde{H}_{\gamma_0}) - \nu(\widetilde{H}_{\gamma_0})) + {\mathrm{o}}_p(1), \end{align}

where

$\widetilde{H}_r(z)\;:\!=\; k_r(z) / \partial_z \psi_X(z)$

and

$\widetilde{H}_r(z)\;:\!=\; k_r(z) / \partial_z \psi_X(z)$

and

$k_r(z) = {\mathrm{e}}^{-rz} - 1$

.

$k_r(z) = {\mathrm{e}}^{-rz} - 1$

.

Appendix B. Estimators of

$p_0$

,

$\boldsymbol{a}^f_{\alpha,K}$

,

$\boldsymbol{a}^F_{\alpha,K}$

, and

$\boldsymbol{a}^{G}_{\alpha,K}$

First, we prepare some notation to give representations of

$p_0$

,

$p_0$

,

$\boldsymbol{a}^f_{\alpha,K}$

, and

$\boldsymbol{a}^f_{\alpha,K}$

, and

$\boldsymbol{a}^F_{\alpha,K}$

in terms of

$\boldsymbol{a}^F_{\alpha,K}$

in terms of

$\nu$

-functionals.

$\nu$

-functionals.

Hereafter we set

$\theta \;:\!=\; (D,\gamma) \in \overline{\Theta} \;:\!=\; \overline{\Theta}_1\times \overline{\Theta}_2$

, and let the true values be

$\theta \;:\!=\; (D,\gamma) \in \overline{\Theta} \;:\!=\; \overline{\Theta}_1\times \overline{\Theta}_2$

, and let the true values be

\begin{align*}\theta_0 \;:\!=\; (D_0,\gamma_0) \in \Theta \;:\!=\; \Theta_1\times \Theta_2,\end{align*}

\begin{align*}\theta_0 \;:\!=\; (D_0,\gamma_0) \in \Theta \;:\!=\; \Theta_1\times \Theta_2,\end{align*}

where

$\Theta_1$

and

$\Theta_1$

and

$\Theta_2$

are open and bounded subsets of

$\Theta_2$

are open and bounded subsets of

$\mathbb{R}_+$

.

$\mathbb{R}_+$

.

We define the following notation. As

$D> 0$

, for

$D> 0$

, for

$\alpha>0$

and

$\alpha>0$

and

$k\in \mathbb{N}_0$

,

$k\in \mathbb{N}_0$

,

\begin{align*}H_p(z;\;\theta) &\;:\!=\; D^{-1} \int_0^z \mathrm{d} y \int_y^\infty {\mathrm{e}}^{-\beta (x-y)}{\mathrm{e}}^{-\gamma (z-x)}\,\mathrm{d} x, \\[5pt] H_{\alpha,k}^f(z;\;\theta)&\;:\!=\; D^{-1}\int_0^z \,\mathrm{d} y \int_y^\infty {\mathrm{e}}^{-\beta (x-y)}{\mathrm{e}}^{-\gamma (z-x)}\varphi_{\alpha,k}(x)\,\mathrm{d} x, \\[5pt] H_{\alpha,k}^F(z;\;\theta)&\;:\!=\; D^{-1}\int_0^z \,\mathrm{d} y \int_y^\infty {\mathrm{e}}^{-\beta (x-y)}{\mathrm{e}}^{-\gamma (z-x)}\Psi_{\alpha,k}(x;\;0)\,\mathrm{d} x.\end{align*}

\begin{align*}H_p(z;\;\theta) &\;:\!=\; D^{-1} \int_0^z \mathrm{d} y \int_y^\infty {\mathrm{e}}^{-\beta (x-y)}{\mathrm{e}}^{-\gamma (z-x)}\,\mathrm{d} x, \\[5pt] H_{\alpha,k}^f(z;\;\theta)&\;:\!=\; D^{-1}\int_0^z \,\mathrm{d} y \int_y^\infty {\mathrm{e}}^{-\beta (x-y)}{\mathrm{e}}^{-\gamma (z-x)}\varphi_{\alpha,k}(x)\,\mathrm{d} x, \\[5pt] H_{\alpha,k}^F(z;\;\theta)&\;:\!=\; D^{-1}\int_0^z \,\mathrm{d} y \int_y^\infty {\mathrm{e}}^{-\beta (x-y)}{\mathrm{e}}^{-\gamma (z-x)}\Psi_{\alpha,k}(x;\;0)\,\mathrm{d} x.\end{align*}

Recall that

$\Psi_{\alpha,k}(x;\;b)$

is given by (2.10) in Definition 2.1. In particular, when

$\Psi_{\alpha,k}(x;\;b)$

is given by (2.10) in Definition 2.1. In particular, when

$D=0$

,

$D=0$

,

\begin{align*}H_p(z;\;\theta) &\;:\!=\; c^{-1}\int_0^z {\mathrm{e}}^{-\gamma (z-x)}\,\mathrm{d} x, \\[5pt] H_{\alpha,k}^f(z;\;\theta)&\;:\!=\; c^{-1}\int_0^z {\mathrm{e}}^{-\gamma (z-x)}\varphi_{\alpha,k}(x)\,\mathrm{d} x, \\[5pt] H_{\alpha,k}^F(z;\;\theta)&\;:\!=\; c^{-1}\int_0^z {\mathrm{e}}^{-\gamma (z-x)}\Psi_{\alpha,k}(x;\;0)\,\mathrm{d} x.\end{align*}

\begin{align*}H_p(z;\;\theta) &\;:\!=\; c^{-1}\int_0^z {\mathrm{e}}^{-\gamma (z-x)}\,\mathrm{d} x, \\[5pt] H_{\alpha,k}^f(z;\;\theta)&\;:\!=\; c^{-1}\int_0^z {\mathrm{e}}^{-\gamma (z-x)}\varphi_{\alpha,k}(x)\,\mathrm{d} x, \\[5pt] H_{\alpha,k}^F(z;\;\theta)&\;:\!=\; c^{-1}\int_0^z {\mathrm{e}}^{-\gamma (z-x)}\Psi_{\alpha,k}(x;\;0)\,\mathrm{d} x.\end{align*}

In this paper we use the convention

\begin{align*}\boldsymbol{H}_{\alpha,K}^{f} = \bigl(H_{\alpha,0}^f, \ldots, H_{\alpha,K}^f\bigr)^\top.\end{align*}

\begin{align*}\boldsymbol{H}_{\alpha,K}^{f} = \bigl(H_{\alpha,0}^f, \ldots, H_{\alpha,K}^f\bigr)^\top.\end{align*}

Then it is straightforward to obtain the following expression by direct computation.

Lemma B.1. It holds that

\begin{align*}p_0 = \nu(H_p(\cdot;\;\theta_0)),\quad a_{\alpha,k}^{f}= \nu\bigl(H_{\alpha,k}^f(\cdot;\;\theta_0)\bigr),\quad a_{\alpha,k}^F = \nu\bigl(H_{\alpha,k}^F(\cdot;\;\theta_0)\bigr).\end{align*}

\begin{align*}p_0 = \nu(H_p(\cdot;\;\theta_0)),\quad a_{\alpha,k}^{f}= \nu\bigl(H_{\alpha,k}^f(\cdot;\;\theta_0)\bigr),\quad a_{\alpha,k}^F = \nu\bigl(H_{\alpha,k}^F(\cdot;\;\theta_0)\bigr).\end{align*}

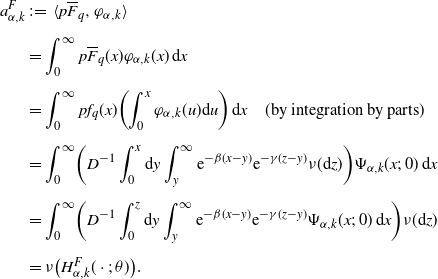

Proof. Use Fubini’s theorem. We shall compute only

$H_{\alpha,k}^F(z;\;\theta)$

:

$H_{\alpha,k}^F(z;\;\theta)$

:

\begin{align*}a^{F}_{\alpha,k}&\;:\!=\; \langle p\overline{F}_{q},\varphi_{\alpha,k}\rangle\\[5pt] &=\int_{0}^{\infty}p\overline{F}_{q}(x)\varphi_{\alpha,k}(x)\,\mathrm{d} x\\[5pt] &=\int_{0}^{\infty}p f_{q}(x)\biggl(\int_{0}^{x}\varphi_{\alpha,k}(u)\mathrm{d}u\biggr)\,\mathrm{d} x \quad \mbox{(by integration by parts)}\\[5pt] &=\int_{0}^{\infty}\biggl(D^{-1}\int_{0}^{x}\mathrm{d}y\int_{y}^{\infty}{\mathrm{e}}^{-\beta(x-y)}{\mathrm{e}}^{-\gamma(z-y)}\nu(\mathrm{d}z)\biggr)\Psi_{\alpha,k}(x;\;0)\,\mathrm{d} x\\[5pt] &=\int_{0}^{\infty}\biggl(D^{-1}\int_{0}^{z}\mathrm{d}y\int_{y}^{\infty}{\mathrm{e}}^{-\beta(x-y)}{\mathrm{e}}^{-\gamma(z-y)}\Psi_{\alpha,k}(x;\;0)\,\mathrm{d} x\biggr)\nu(\mathrm{d}z)\\[5pt] &=\nu\bigl(H^{F}_{\alpha,k}(\cdot;\;\theta)\bigr).\end{align*}