Preface

Over the past decade, deep learning has attracted considerable interest, primarily due to its exceptional performance across a range of application domains, with image recognition and natural language processing standing out as two of the most notable examples. Deep learning algorithms possess the ability to learn complex, nonlinear relationships from large volumes of data. Unlike traditional mathematical or statistical models, which often struggle in such environments, deep learning models excel at uncovering complex patterns and making predictions. The capacity to manage and learn from large volumes of data has made deep learning models a transformative technology across industries like healthcare, finance, entertainment, and many others.

Given its successful applications in other fields, deep learning has also become a natural candidate for applications to quantitative trading, as trading firms and investment managers continuously seek innovative ways to uncover “alpha,” or excess returns. With the rise of electronic trading, exchanges now process billions of messages daily, generating vast amounts of data well suited for deep learning algorithms. Additionally, investors also have access to a growing range of alternative data sources, such as mobile app downloads, social media trends, and search engine activity (e.g., Google Trends), which can be used to further improve decision-making. As a result, deep learning techniques are increasingly becoming powerful tools for quantitative researchers and traders, enabling more sophisticated strategies and potentially higher returns.

A significant body of research has explored the diverse financial applications of deep learning, including areas such as alpha generation, time-series forecasting and portfolio optimization. The goal of this Element is to weave these disparate threads together, placing a particular emphasis on how deep learning algorithms can be leveraged to develop quantitative trading strategies and systems. Whether an experienced quantitative trader aiming to enhance strategies, a data scientist exploring opportunities within the financial sector, or a student eager to delve into cutting-edge financial technology, the reader of this Element should come away with a comprehensive understanding of how deep learning is transforming the landscape of quantitative trading. By combining theoretical foundations with practical applications, we seek to equip readers with the insights and tools necessary to excel in this rapidly evolving domain. Our objective is to navigate the complexities of the field while inspiring innovation in the integration of deep learning within quantitative finance.

To promote reproducibility and enhance readers’ understanding of the algorithms discussed in this Element, we have created a dedicated GitHub repository.Footnote 1 This repository contains many of the experiments presented in the book, and it includes everything from fundamental data processing pipelines to implementations of cutting-edge deep neural networks. By providing these resources, we aim to empower readers to apply the concepts and techniques in practical, real-world settings. This repository is designed to be user-friendly and accessible, and it includes step-by-step examples and demonstrations. All deep learning models are built using PyTorch, a widely used and flexible deep learning framework. Accordingly, readers can easily experiment with and extend these implementations. Whether readers are looking to replicate the included experiments, refine the models, or use the provided pipelines as foundations for their own projects, the repository offers a hands-on platform to bridge theory and practice. Our commitment to transparency and accessibility ensures that readers can not only learn but also actively engage with and contribute to the evolving field of quantitative finance powered by deep learning.

1 Introduction

Quantitative trading boasts a rich and fascinating history, with its origins dating back to the groundbreaking work of Louis Bachelier in 1900. In his seminal thesis, Bachelier introduced the concept of Brownian motion as a framework for modeling the stochastic behavior of financial price series. This pioneering work established the basis for the mathematical modeling of financial markets and set the stage for modern quantitative finance (Bachelier, Reference Bachelier1900). Over the years, the field has undergone remarkable evolution, propelled by progress in mathematics, statistics, and computational advancements. From the introduction of fundamental theories like the Black-Scholes model in the 1970s to the emergence of algorithmic trading in the late twentieth century, quantitative trading has consistently been at the forefront of financial innovation. Key developments have been documented in works such as Cesa (Reference Cesa2017), which offers a detailed exploration of quantitative finance’s historical trajectory and major milestones.

As computational power and data availability have both increased, the field has expanded further, incorporating machine learning and deep learning techniques into its toolkit. Today, quantitative trading represents a dynamic intersection of finance, mathematics, and computer science, continuing to evolve as new methods and technologies emerge. Experts from diverse fields have collaborated with a common goal: to optimize financial returns while minimizing the inherent risks of trading. This shared ambition has fueled the evolution of quantitative trading strategies, which harness the power of mathematical and computational models to analyze and interpret financial data.

Traditionally, statistical time-series models have served as the cornerstone of predictive signal generation in quantitative trading. These models, such as ARIMA and GARCH, have proven effective in capturing trends and volatility in financial time-series data. However, such models are often constrained by their linear nature and the stringent assumptions, such as stationarity and normality, that they impose upon the data. Given the inherently complex and nonlinear behavior of financial markets, these limitations can lead to suboptimal performance, particularly in dynamic and unpredictable market conditions. To address these challenges, practitioners have historically relied upon manually crafted features to enhance the predictive power of their models. By engineering features that capture specific market dynamics, such as momentum, mean reversion, and volatility clusters, researchers aim to approximate the underlying complexity of financial systems. However, this process is labor-intensive, requiring significant domain expertise and time. Moreover, manual feature engineering is susceptible to human bias, potentially introducing or overlooking critical patterns or relationships in the data.

The increasing demand for more robust and scalable solutions has underscored the need for advanced methodologies capable of identifying and leveraging nonlinear relationships within financial data. Deep learning, a specialized branch of machine learning, utilizes multi-layered neural networks to autonomously learn and uncover meaningful patterns within large and complex datasets. The core advantage of deep learning is its capacity to learn hierarchical representations of data. By progressively extracting features from raw inputs, deep learning models are capable of capturing complex relationships and subtle patterns that traditional statistical methods often fail to detect. These capabilities make them especially well suited for addressing the complexities of financial markets, which are characterized by high volatility, intricate interdependencies, and noisy data. Specifically, deep learning offers several distinct advantages: It can handle both structured and unstructured data, such as news articles and social media sentiment; it can adapt to changing market conditions and regimes; it can uncover complex patterns as more complex data increasingly requires more complex modeling techniques; it can be used for a range of strategy types, from high-frequency execution problems to long-term portfolios optimization.

This Element delves deeply into the transformative role of deep learning in modern quantitative trading, offering a thorough examination of how this advanced technology is transforming the landscape of financial markets. Through this exploration, we aim to showcase how deep learning models excel at automating complex feature extraction processes and uncovering patterns within vast volumes of financial data. Through their ability to do so, deep learning models drive more informed, precise, and effective trading strategies. Our objective is to guide readers, whether researchers, data scientists, or traders, through the practical applications and theoretical underpinnings of deep learning in quantitative trading. This Element seeks to demonstrate how the unmatched computational power and adaptability of deep learning can be leveraged to develop applications for real-world, high-stakes financial trading environments. Readers will obtain a meaningful understanding of how these models can be applied to automate decision-making, enhance predictive accuracy, and optimize trading performance in the ever-evolving financial markets.

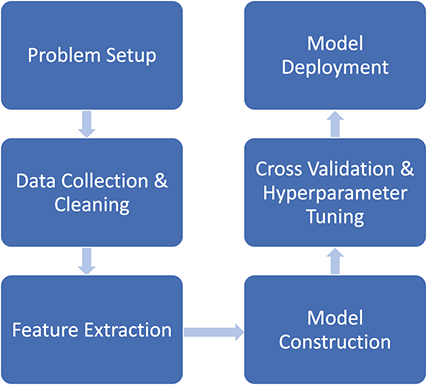

The Element is split into two parts: Foundations and Applications. In the first part, we cover the fundamentals of financial time-series including statistics and hypothesis testing. Financial data, like any other type of data, has its own characteristics. Accordingly, a good understanding of a financial dataset’s underlying statistics is the basis for any financial analysis. We then introduce the concept of supervised learning and deep learning models. These concepts range from basic fully connected layers to the attention mechanism and transformer architectures, which excel at capturing long-range dependencies in structured datasets. Despite the significant advancements in deep learning, deep networks frequently encounter challenges like overfitting, when models excel on training data but struggle to generalize to new, unseen data. To address this, we present a complete workflow for developing deep learning algorithms for quantitative trading. This process includes essential steps like data collection, exploratory data analysis (evaluating characteristics of the data, such as distribution and stationarity), and cross-validation techniques tailored specifically for financial data. These steps are critical for building models that are robust and reliable.

In the second part of this Element, we focus on applying deep learning algorithms to various financial problems. One of the most fundamental tasks in quantitative trading is generating predictive signals. We explore various deep learning architectures for this purpose, showcasing how these networks can be leveraged to predict market movements. Building on this foundation, we delve into more advanced frameworks where deep networks are adopted to enhance time-series momentum and cross-sectional momentum trading strategies. Further, we discuss portfolio optimization and present methods to optimize portfolio weights from market inputs that form an end-to-end framework. This bypasses the intermediate requirements of estimating returns and constructing a covariance matrix of returns, processes that are often difficult to implement in practice.

Alongside our exploration of deep learning techniques, this Element discusses the nature and intricacies of financial data itself. To provide a detailed perspective, we introduce the operational mechanisms of modern securities exchanges, illustrating how financial transactions occur and the ways in which high-frequency microstructure data, such as order book updates and trade executions, are generated. Additionally, we analyze the unique characteristics of several main asset classes, including equities, bonds, commodities, and cryptocurrencies, shedding light on the distinct challenges and opportunities they each present for deep learning applications. Throughout this Element, we include code scripts to highlight important concepts, and we provide a dedicated GitHub repositoryFootnote 2 to further demonstrate these ideas.

An Outline of the Element

This Element contains two parts: Foundations and Applications. The Foundations part contains Sections 2, 3 and 4, in which we introduce the fundamentals of financial time-series and deep learning algorithms. The Applications contains Sections 5, 6, and 7, in which we discuss prediction, portfolio optimization, trade execution and real-world applications.

Section 2 discusses the statistics frequently used in the analysis of financial time-series, including returns, data distributions, hypothesis testing, statistical moments, serial covariance, correlation, and statistical time-series models such as AR and ARMA. This section also introduces the notions of “alpha” and “beta” and examines the phenomenon of volatility clustering.

Section 3 introduces supervised learning and its primary components, including loss functions and evaluation metrics. We then introduce neural networks, starting with the canonical fully connected layers, convolutional and recurrent layers. Finally, we explore some state-of-the-art networks, including WaveNet, encoder-decoders, and transformers.

Section 4 presents a complete training workflow from the very first step of data collection through the final model deployment. We discuss the problem of overfitting and introduce cross-validation for hyperparameter tuning. We also include a discussion of various popular model pipelines so that readers can choose the most appropriate platform for their respective applications.

Section 5 introduces classical quantitative strategies such as time-series momentum and cross-sectional momentum strategies, and shows how they can be enhanced with deep learning methods. In particular, we explore networks that directly output trade positions and are end-to-end optimized for Sharpe ratio or other performance metrics.

Section 6 focuses on risk management and portfolio optimization. We demonstrate how deep learning models can help better forecast risk measures such as volatility. We also look into end-to-end deep learning frameworks for portfolio optimization, bypassing the need to estimate returns or construct a covariance matrix for classical mean-variance problems.

Section 7 introduces high-frequency microstructure data. We demonstrate how bespoke hybrid-networks can serve to forecast future price trends and exploit additional structure in limit order books. Additionally, we discuss various promising applications including the adoption of reinforcement learning for trade execution and generative modeling for financial data.

Section 8 brings together the insights and knowledge presented throughout this Element, summarizing the key takeaways from our exploration of deep learning and quantitative trading. Looking ahead, we discuss emerging trends and explore future possibilities where deep learning might bring innovative transformations to financial markets.

Part I: Foundations

2 Fundamentals of Financial Time-Series

Financial time-series analysis is an indispensable tool in understanding the ever-changing nature of financial markets. It involves the study of certain data points collected or recorded at specific time intervals, such as daily stock prices. This analysis is crucial for identifying trends, modeling market behaviors, and making informed decisions in trading, risk management, and investment. This section explores the fundamental concepts of statistics used in such analyses, including returns, distributions, moments, hypothesis testing, serial covariance, various time-series models, and more. These concepts form the basis of financial time-series modeling and provide the foundation to move to more complex models later in the Element.

2.1 Returns

Returns are a key metric in the field of finance, playing an important role in evaluating investment performance over time. They reflect the profit or loss achieved relative to the initial value of an investment, demonstrating insights into the potential profitability and risks associated with different traded financial assets, including stocks, bonds, mutual funds, and other instruments. By calculating and analyzing returns, investors, analysts, and portfolio managers can assess the effectiveness of their strategies, compare diverse investment options, and make data-driven decisions to enhance trading performance.

There are several different ways to calculate financial returns, with simple returns and logarithmic (log) returns being the most common. Simple returns calculate the percentage change in an asset’s price between two consecutive periods. They are straightforward to calculate and understand, which makes them a widely used tool for routine financial analysis. In addition, simple returns are often used to calculate portfolio returns (which will be defined in later sections). However, simple returns have limitations, particularly when dealing with long-term investments or compounding returns.

Logarithmic returns, on the other hand, calculate the natural logarithm of the ratio of consecutive prices. This method provides a time-additive measure, meaning that the returns over multiple periods can be summed up to obtain the total return, which is particularly useful for continuous compounding contexts. Logarithmic returns are often more statistically desirable due to their properties, such as normality and symmetry, which make them more suitable for sophisticated financial models and risk assessments. The motivation for using those two forms becomes apparent when calculating the cumulative return of a security. For a single time step, we can define both returns as follows:

(1)

(1)

where  denotes the price of a security at time

denotes the price of a security at time  . The aforementioned can easily be generalized for returns over multiple time steps from

. The aforementioned can easily be generalized for returns over multiple time steps from  to

to  .

.

Understanding and analyzing financial returns is crucial for several reasons. First, returns directly impact an investor’s wealth and financial planning, as they determine the growth of investments over time. Second, returns are used when assessing investment risks, and effective risk control is the key to ensuring long-term investment success. Third, analyzing historical returns helps investors identify trends and patterns, informing future investment decisions and strategy development. Finally, financial institutions and fund managers rely heavily upon return analysis to manage large portfolios and ensure they meet their performance benchmarks. By examining returns, they can allocate assets more effectively, diversify their portfolios, and carry out risk management strategies that can protect profits against adverse market movements.

In summary, financial returns are a cornerstone of investment analysis and decision-making. They provide a complete view of the performance and risk of financial assets, guiding investors and financial professionals in their pursuit of optimal investment strategies and wealth maximization. Understanding the different methods of calculating returns is important for anyone involved in the financial world. In many of the data-driven examples that we cover in this Element, a future return over a specific horizon serves as the target of a predictive supervised learning model. It reflects the direction and extent of the expected future price movement and plays a major role in portfolio optimization, which will be discussed more in later sections.

2.2 Distributions of Financial Returns

Loosely speaking, a distribution describes the way in which values of a random variable are spread or dispersed. Distributions are the foundation for the domains of probability and statistics, and distributions can be either discrete, where data points can take on values from a finite or a countable set, or continuous, where data points can take on any value within a given range. Understanding distributions is useful for making inferences about populations based on samples, assessing probabilities, and conducting various statistical tests.

Mathematically, we represent the distribution of a discrete variable by a probability mass function (PMF) and that of a continuous variable by a probability density function (PDF). The PMF simply indicates the probabilities of different finite or countable outcomes, and the PDF presents how the probability of a random variable taking values in a specific range is distributed. The key properties of PMFs or PDFs are that they are nonnegative and sum to one over the entire space of possible values. Taking a continuous variable  with the PDF

with the PDF  as an example, the probability that

as an example, the probability that  lies within the interval

lies within the interval  is determined by the integral of

is determined by the integral of  over that range:

over that range:

(2)

(2)

It is important to understand the concept of the distribution of financial returns as it gauges the quality and risk of investment performance. In practice, financial returns do not typically follow a normal distribution, which would suggest they tend not to be well behaved. Instead, they exhibit characteristics, such as heavy tails which indicate that extreme values (large gains or losses) are more frequent than would be predicted by a normal distribution.

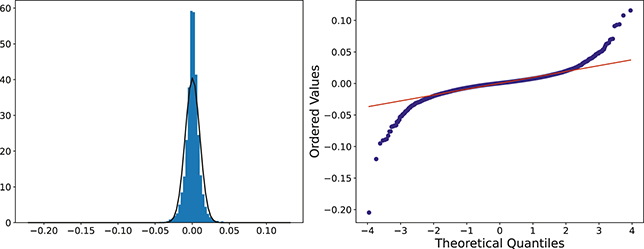

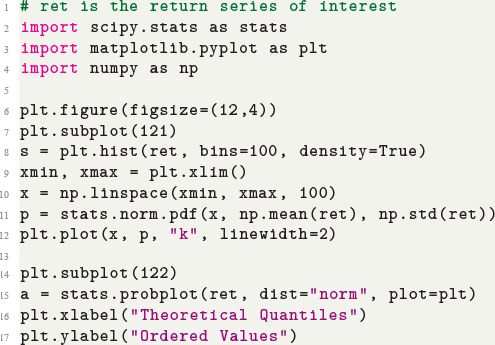

There are several ways to understand a distribution. The most straightforward way is to use histograms to visually inspect the data distribution. For example, the left plot of Figure 1 depicts the histogram for the simple daily returns of Standard & Poor’s 500 (S&P500) since its creation. The distribution is bell-shaped and appears similar to a normal (Gaussian) distribution. However, upon inspection, this distribution exhibits fatter tails and a sharper peak compared to a normal distribution with the same mean and standard deviation (plotted in black).Footnote 3

Figure 1 Left: histogram for the return distribution; Right: QQ-plot.

Figure 1Long description

In the left graph, the x-axis ranges from minus 0.20 to 0.10, and the y-axis ranges from 0 to 60 with increments of 10. The data are follow: (minus 0.05, 0), (0.00, 40), (0.05, 0). In the right graph, the x-axis represents Theoretical Quantiles ranging from minus 4 to 4 and the y-axis represents Ordered values ranging from minus 0.20 to 0.10. A line drawn through the points (minus 4, minus 0.05), (0, 0.00), (4, 0.04). All values are approximate.

QQ-plot (quantile-to-quantile plot) is another popular tool to check if a data distribution is normal. A QQ-plot is made by plotting one set of quantiles against another set of quantiles. A quantile denotes an input value, in this case a return, such that a certain fraction (say 90%) of the data are less than or equal to this value (in which case we call it the 90% quantile). A straight line would be expected if two sets of quantiles are from the same distribution. The right of Figure 1 is the QQ-plot for the return distribution of the S&P 500 versus the assumed normal distribution. We can observe that the points align along a straight line in the central portion of the figure, but curve off at the two ends. In general, a QQ-plot like this indicates that extreme values are more likely to occur than the assumed normal distribution. Code to create a histogram and a QQ-plot in Python is shown next:

Code 1.1

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

Empirical studies of financial markets have shown that the distribution of returns is often better fit by distributions such as the Student’s t-distribution, which better accounts for the heavy tails, or the Generalized Error Distribution (GED). These distributions offer a more accurate depiction of the probability of extreme events, and consequently better model financial time-series. We need to be aware of such properties because a higher likelihood of extreme events means that financial models have a higher potential for significant losses.

Overall, a good understanding of return distributions helps with financial modeling, risk assessment, and strategic decision-making. By recognizing that returns are not normally distributed and accounting for the actual distributional characteristics, investors and analysts can develop more robust models that better capture the risks and potential rewards of their investments. This knowledge allows for more effective portfolio diversification, hedging strategies, and overall risk management practices, ultimately leading to more informed and potentially profitable investment decisions.

2.3 Statistical Moments

Statistical moments are sets of parameters used to describe a distribution. In general, we can define the  -th central moment of a random variable

-th central moment of a random variable  as:

as:

(3)

(3)

for  and

and  . Typically, attention is given to the first four moments – mean (or expected value), variance, skewness, and kurtosis – as they capture a distribution’s central tendency, spread, asymmetry, and peakedness, respectively. Statistical moments help us understand the behavior of a distribution and make predictions. For example, a normal distribution can be specified by giving a mean and standard deviation. However, these two moments alone might not be enough to fully describe a return distribution. As an example, the return distribution in Figure 1 exhibits heavier tails and a more pronounced peak than a normal distribution. In this case, we need to check higher moments of the distribution to better understand the data.

. Typically, attention is given to the first four moments – mean (or expected value), variance, skewness, and kurtosis – as they capture a distribution’s central tendency, spread, asymmetry, and peakedness, respectively. Statistical moments help us understand the behavior of a distribution and make predictions. For example, a normal distribution can be specified by giving a mean and standard deviation. However, these two moments alone might not be enough to fully describe a return distribution. As an example, the return distribution in Figure 1 exhibits heavier tails and a more pronounced peak than a normal distribution. In this case, we need to check higher moments of the distribution to better understand the data.

In statistics, skewness and kurtosis are the normalized third and fourth central moments. Skewness measures the asymmetry of data about its mean. There are two types of skewness: positive skew and negative skew. A symmetrical distribution, such as a normal distribution, has no skewness. However, a distribution that has larger values on the right tail is positively skewed. On the contrary, a negatively skewed distribution has larger values in the left tail that are further from the mean than those of the left tail.

In finance, skewness may stem from diverse market forces. Investor sentiment can lead to asymmetrical buying or selling pressures as market participants overreact to news or trends. Economic news can also introduce sudden, unidirectional shocks to asset prices as markets rapidly adjust to new information. Market microstructure might also contribute to skewness when imbalances in order flow, liquidity constraints, or trading mechanisms create price distortions. There are many other possible causes for deviations from a normal distribution in the returns.

The skewness of a return distribution can typically inform the reward profile of a security or strategy. A canonical example of a strategy that is negatively skewed is a reversion strategy. We can expect many small positive rewards when assets revert as expected, but we can also suffer large losses if reversion does not occur say due to an unexpected news event. Selling options and VIX futures are other examples of strategies with negatively skewed return distributions. Vice versa, a positively skewed return distribution typically corresponds to many small losses with a few large gains – a canonical example being momentum strategies. The most favorable type of skewness depends upon the risk preferences of investors.

Kurtosis is the fourth normalized statistical moment, describing the tail and peak of a distribution. In particular, kurtosis informs us whether a distribution includes more extreme values than a normal distribution. All normal distributions, regardless of mean and variance, have a kurtosis of 3. If a distribution is highly peaked and has fat tails, its kurtosis is greater than 3, and, vice versa, a flatter distribution has a kurtosis lesser than 3. Excess kurtosis can be attributed to market shocks, economic crises, and other rare but impactful events that significantly affect asset prices.

2.4 Statistical Hypothesis Testing

Hypothesis testing is another important concept in statistics, as it offers a systematic framework for making decisions and drawing conclusions about a population using sample data. It is widely adopted in several fields, including natural science, economics, psychology, and finance, where it is used to evaluate hypotheses and determine the validity of claims or theories. For example, we have already mentioned the fact that financial returns can have fat tails compared to a normal distribution. To objectively assess this, we resort to hypothesis testing which provides a formal framework for making inferences and offers a structured method for evaluating claims. Consequently, this allows researchers and analysts to draw conclusions with a quantifiable level of confidence. By using statistical techniques and predefined criteria, it also eliminates subjective biases and ensures that decisions are conditioned on empirical evidence rather than intuition or guesswork.

The fundamental concept of hypothesis testing involves using sample data to evaluate the evidence against a null hypothesis ( ), which functions as the default or baseline assumption. The objective is to prove the alternative hypothesis (

), which functions as the default or baseline assumption. The objective is to prove the alternative hypothesis ( ), which constitutes the presence of a difference from the default assumption. The process of hypothesis testing involves several key steps. First, we need to define the null hypothesis and the alternative hypothesis. For instance, in a test to determine whether the distribution of returns is normal, the null hypothesis might state that the return distribution follows a normal distribution, while the alternative hypothesis might posit that the return distribution violates the assumption of normality.

), which constitutes the presence of a difference from the default assumption. The process of hypothesis testing involves several key steps. First, we need to define the null hypothesis and the alternative hypothesis. For instance, in a test to determine whether the distribution of returns is normal, the null hypothesis might state that the return distribution follows a normal distribution, while the alternative hypothesis might posit that the return distribution violates the assumption of normality.

We then need to select a significance level ( ), typically 0.05, which delineates the probability of erroneously rejecting the null hypothesis when it is in fact true. The value of

), typically 0.05, which delineates the probability of erroneously rejecting the null hypothesis when it is in fact true. The value of  reflects the strength of the evidence for rejection, and thus a small

reflects the strength of the evidence for rejection, and thus a small  imposes a requirement of strong evidence for the null hypothesis to be rejected. In addition, it is necessary to select an appropriate test statistic in accordance with the nature of the data and the hypothesis under examination. Popular test statistics include the z-score, t-score, F-statistic, and chi-square statistic.Footnote 4 Following is a complete example of one-sample hypothesis testing to determine whether the mean of a population is zero. Suppose we have a random sample

imposes a requirement of strong evidence for the null hypothesis to be rejected. In addition, it is necessary to select an appropriate test statistic in accordance with the nature of the data and the hypothesis under examination. Popular test statistics include the z-score, t-score, F-statistic, and chi-square statistic.Footnote 4 Following is a complete example of one-sample hypothesis testing to determine whether the mean of a population is zero. Suppose we have a random sample  from some unknown distribution. We assume that the sample mean is approximately normally distributed for large

from some unknown distribution. We assume that the sample mean is approximately normally distributed for large  , and we want to test the null and alternative hypotheses:

, and we want to test the null and alternative hypotheses:

(4)

(4)

where  is the true mean of the population. To calculate the test statistic, we use a t-statistic with

is the true mean of the population. To calculate the test statistic, we use a t-statistic with  degrees of freedom:

degrees of freedom:

(5)

(5)

where  and

and  are the sample mean and standard deviation. Under

are the sample mean and standard deviation. Under  , this statistic approximately follows a t-distribution with

, this statistic approximately follows a t-distribution with  degrees of freedom.

degrees of freedom.

After computing the test statistic using sample data, we derive a value that can be compared against a critical value for a given alpha. The probability of observing a test statistic, under  , that is more extreme than the one we computed from our data is called the

, that is more extreme than the one we computed from our data is called the  -value. The

-value. The  -value decides the statistical significance of our results compared to the null hypothesis. In the previous example, we can find

-value decides the statistical significance of our results compared to the null hypothesis. In the previous example, we can find  where

where  is the observed value of the statistic, and

is the observed value of the statistic, and  denotes a random variable following the t-distribution with

denotes a random variable following the t-distribution with  degrees of freedom. If the resulting

degrees of freedom. If the resulting  -value is smaller than the significance level, for example,

-value is smaller than the significance level, for example,  , then we can say the test result is significant, indicating strong evidence against the null hypothesis.

, then we can say the test result is significant, indicating strong evidence against the null hypothesis.

In the previous section, we use graphical tools to assess data distributions but we can now also use statistical hypothesis testing to validate data properties. For instance, the Jarque-Bera test can be utilized to assess the validity of the normality assumption. This widely recognized statistical method evaluates whether the sample data skewness and kurtosis are consistent with those expected in a normal distribution, thereby determining if the return distribution adheres to normality.

2.5 Serial Covariance, Correlation, and Stationarity

For time-series forecasting, we make predictions based on historical observations from previous time stamps. While increments in financial time-series are close to independent random variables, and are indeed often modeled by stochastic processes such as Geometric Brownian Motion (GBM), it is still possible to identify and exploit small dependencies to make predictions. We can measure such dependence with serial covariances (autocovariances) or serial correlations (autocorrelations).

Serial covariance refers to the measure of how two variables change together over time within a time-series. In the context of financial time-series, it specifically measures the covariance between different observations of the same financial variable at different points in time. Intuitively, autocovariance tells us how two instances of a time-series  at different time points move together. Understanding serial covariance is beneficial for identifying patterns and predicting future values based on historical data. For example, if the price of a stock today is positively correlated with its price yesterday, this might indicate a future upward trend.

at different time points move together. Understanding serial covariance is beneficial for identifying patterns and predicting future values based on historical data. For example, if the price of a stock today is positively correlated with its price yesterday, this might indicate a future upward trend.

Correlation quantifies both the magnitude and the orientation of the linear association between two time-series. In contrast to covariance, correlation is both standardized and dimensionless, offering a uniform metric for assessing the extent to which two variables vary together. The correlation coefficient spans from -1 to 1, where 1 signifies a flawless positive linear association, -1 denotes a perfect negative linear relationship, and 0 implies the absence of any linear relationship. Formally, we can define covariance and correlation as:

(6)

(6)

Correlation is essential for many applications in financial time-series analysis. By evaluating the extent to which two assets fluctuate together, investors are able to design portfolios that reduce risk while optimizing returns. For instance, when two assets exhibit low or negative correlations, a portfolio combining the two can achieve lower overall volatility compared to portfolios consisting of highly correlated assets. Correlation analysis is also used for detecting market inefficiencies and arbitrage opportunities. For example, if two assets are expected to be highly correlated due to economic or financial reasons but deviate significantly at some point, one could speculate that this deviation will shrink again.

We can check how a time-series relates to previous observations (at various time lags) using Autocorrelation Function (ACF) plots and Partial Autocorrelation Function (PACF) plots. The ACF measures the correlation between a time-series and its own lagged (i.e., past) values. It indicates the degree to which past values of a series influence its current values, providing insights into the internal structure and patterns of the data. The ACF is especially effective in detecting trends, seasonal patterns, and various cyclical behaviors within a dataset. Mathematically, the ACF at lag  for a time-series

for a time-series  is defined as:

is defined as:

(7)

(7)

where  is the covariance between

is the covariance between  and

and  , and

, and  is the variance of the time-series. The values of the ACF span from -1 to 1, where values approaching 1 signify a robust positive correlation, those nearing -1 indicate a strong negative correlation, and values around 0 imply minimal to no correlation. A correlogram depicts the autocorrelation of a time-series as a function of time lags. This plot can help identify the appropriate model for time-series forecasting, such as an Autoregressive Moving Average model (ARMA), in which the autocorrelation structure guides the selection of model parameters.

is the variance of the time-series. The values of the ACF span from -1 to 1, where values approaching 1 signify a robust positive correlation, those nearing -1 indicate a strong negative correlation, and values around 0 imply minimal to no correlation. A correlogram depicts the autocorrelation of a time-series as a function of time lags. This plot can help identify the appropriate model for time-series forecasting, such as an Autoregressive Moving Average model (ARMA), in which the autocorrelation structure guides the selection of model parameters.

The PACF serves as an additional instrument in time-series analysis, quantifying the correlation between a time-series and its lagged values while also eliminating the linear effects of intermediate lags. Unlike the ACF, which includes the cumulative effect of all previous lags, the PACF isolates the direct effect of a specific lag. For instance, the PACF at lag  measures the correlation between

measures the correlation between  and

and  after removing the effects of lags 1 through

after removing the effects of lags 1 through  . This allows for a clearer understanding of the underlying relationship at each specific lag, making it easier to identify the appropriate number of lags to include in an autoregressive model.

. This allows for a clearer understanding of the underlying relationship at each specific lag, making it easier to identify the appropriate number of lags to include in an autoregressive model.

Mathematically, we can define the PACF at lag  as the correlation between

as the correlation between  and

and  that is not accounted for by their mutual correlation with

that is not accounted for by their mutual correlation with

. We can obtain PACF values by fitting a linear model with

. We can obtain PACF values by fitting a linear model with  and the regressors standardized:

and the regressors standardized:

(8)

(8)

where  is the PACF value for lag

is the PACF value for lag  , and ranges from

, and ranges from  to 1. With standardization, the regression slopes become the partial correlation coefficient, as correlation is effectively the slope we get when both the response and predictors have been reduced to dimensionless “z-scores.” The PACF plot is used in conjunction with the ACF plot to identify the order of an autoregressive (AR) model. While the ACF helps in understanding the overall autocorrelation structure, the PACF helps pinpoint the specific lags that should be included in the AR component of an ARMA model, ensuring a more accurate estimation.

to 1. With standardization, the regression slopes become the partial correlation coefficient, as correlation is effectively the slope we get when both the response and predictors have been reduced to dimensionless “z-scores.” The PACF plot is used in conjunction with the ACF plot to identify the order of an autoregressive (AR) model. While the ACF helps in understanding the overall autocorrelation structure, the PACF helps pinpoint the specific lags that should be included in the AR component of an ARMA model, ensuring a more accurate estimation.

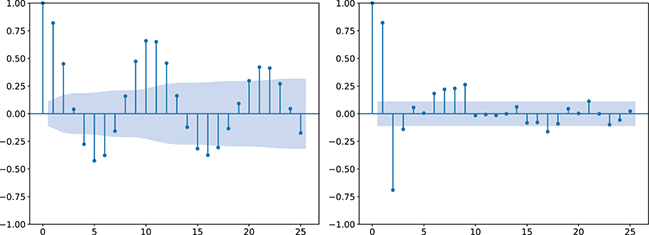

In summary, the ACF and PACF are powerful tools that enable a deeper understanding of time-series data, guiding the development of robust and effective forecasting models. Their combined use allows for the precise identification of temporal structures, leading to improved predictions and better decision-making in fields where time-series data is prevalent. Figure 2 shows an example of ACF and PACF plots for the same underlying data. The shaded area in the plot represents an approximate confidence interval around zero correlation. In other words, it is a visual guide for checking which autocorrelation (or partial autocorrelation) lags are statistically significant from zero. We can make these plots using the following code:

Figure 2 Left: ACF plot; Right: PACF plot.

Figure 2Long description

In the left graph, the x-axis ranges from 0 to 25 with increments of 5, and the y-axis ranges from minus 1.00 to 1.00. A horizontal line is drawn at 0.00 on the y-axis, with several vertical lines extending upward and downward from it. In the right graph, the x-axis ranges from 0 to 25 with increments of 5, and the y-axis ranges from minus 1.00 to 1.00. A horizontal line is drawn at 0.00 on the y-axis, with multiple vertical lines extending both above and below the horizontal line.

Code 1.2

1

2

3

4

5

6

7

Next, we discuss another concept that is commonly used in time-series known as stationarity. Stationarity refers to the statistical property of a time-series where its key characteristics, such as mean, variance, and autocovariance structure, remain constant over time. This consistency makes stationary time-series easier to analyze and model, as their behavior is predictable and stable. In financial markets, where data often exhibit complex patterns, achieving stationarity is helpful for accurate modeling, forecasting, and risk management.

There are two forms of stationarity: strict stationarity and weak stationarity. We say that a time-series process is strictly stationary if the joint distribution  is identical to the joint distribution

is identical to the joint distribution  for all collections

for all collections  and separate values

and separate values  . However, this assumption is very restrictive and very few real-world examples meet this requirement. Differently, we say that a time-series process is weakly stationary if:

. However, this assumption is very restrictive and very few real-world examples meet this requirement. Differently, we say that a time-series process is weakly stationary if:

where the mean of a time-series is constant and finite,

where the mean of a time-series is constant and finite,- where the variance of a time-series is constant and finite,

the autocovariance and autocorrelation functions only depend on the lag:

(9)

A considerable number of statistical and econometric models operate under the assumption that the underlying time-series remains stationary. These models depend on the stability of statistical characteristics to generate precise forecasts. In finance, stationarity ensures that historical risk measures, such as volatility and correlation, remain relevant for future periods. In practice, financial time-series frequently display non-stationary characteristics as a result of trends, seasonal patterns, and structural shifts. To achieve stationarity, analysts use various techniques. For example, they might use differencing to subtract previous observation from the current observation with the aim of removing trends and achieving a stationary series. Additionally, they might remove a deterministic trend component from a series (detrending) or apply transformations like logarithms to stabilize the variance.

2.6 Time-Series Models

We have introduced ACF and PACF which can be used to determine the order of AR and ARMA models. But what exactly are these models? In simple words, these are classical time-series models that form a crucial aspect of analyzing sequential data, particularly in fields such as finance, economics, and environmental science. By identifying patterns and correlations in historical price data, we can employ time-series models to develop quantitative trading strategies by exploiting patterns for profit. AR models, for instance, can help in detecting momentum or mean-reversion patterns, which are commonly used in algorithmic trading.

Beyond financial markets, time-series models are vital for economic policy and planning. Central banks and governmental bodies employ these models to predict key economic metrics, including GDP expansion, inflation levels, and unemployment figures. Accurate forecasts help make informed policy decisions that can stabilize the economy and promote growth. Within the spectrum of time-series models, the Autoregressive model (AR), moving average model (MA), and Autoregressive Moving Average model (ARMA) models are among the most fundamental due to their simplicity and effectiveness. These models are capable of capturing the underlying patterns and dynamics of time-series data, making them powerful tools for analysts and researchers aiming to model and forecast temporal data accurately.

The AR is among the most basic and extensively employed time-series models. It describes the current value of a series as a linear aggregate of its past values combined with an independent random error component. If an AR model takes  previous observations, we denote the model as AR(

previous observations, we denote the model as AR( ) and its functional form is given as follows:

) and its functional form is given as follows:

(10)

(10)

where  is the value at current time stamp

is the value at current time stamp  ,

,  are the model parameters that represent the effects of past values on the output value, and

are the model parameters that represent the effects of past values on the output value, and  is an error term. For a given order

is an error term. For a given order  , we can fit the model and find the optimal coefficients

, we can fit the model and find the optimal coefficients  in the same way as we would fit a linear regression, with the lagged values

in the same way as we would fit a linear regression, with the lagged values  being the predictors and

being the predictors and  the target. In order to decide which order

the target. In order to decide which order  to use, we can look at the PACF plot. For example, considering the time-series presented in Figure 2, the PACF suggests that an AR(3) model would probably capture most of the dependence, while it might be useful to consider an AR(9) model to capture further dependence.

to use, we can look at the PACF plot. For example, considering the time-series presented in Figure 2, the PACF suggests that an AR(3) model would probably capture most of the dependence, while it might be useful to consider an AR(9) model to capture further dependence.

The AR model captures how the current observations depend on their past values, making it suitable for modeling time-series with strong autocorrelations. This model is particularly effective when the underlying process is driven by its own past values, which can be the case for stock prices or interest rates. For example, an AR( ) model, where the output depends only on the immediate past observation, is defined as:

) model, where the output depends only on the immediate past observation, is defined as:

(11)

(11)

where the model suggests that the current value of the time-series is influenced directly by the observation at time  .

.

Differently than the AR model, the MA model represents the current value of a time-series as a linear combination of its previous error terms. The MA model of order  , symbolized as MA(

, symbolized as MA( ), is defined as:

), is defined as:

(12)

(12)

where  is the mean of the series,

is the mean of the series,  are error terms,

are error terms,  are the model parameters that represent the influence of past errors on the current value. The MA model captures the influence of past shocks or disturbances on the current observation, making it useful for modeling time-series with short-term dependencies. This model is effective when the series is subject to random shocks that have a lasting but diminishing impact over time. For instance, an MA(

are the model parameters that represent the influence of past errors on the current value. The MA model captures the influence of past shocks or disturbances on the current observation, making it useful for modeling time-series with short-term dependencies. This model is effective when the series is subject to random shocks that have a lasting but diminishing impact over time. For instance, an MA( ) model defines that the observation at time

) model defines that the observation at time  is only influenced by the immediate past error:

is only influenced by the immediate past error:

(13)

(13)

although, in practice, we can include several terms to model output. To decide the order of a MA model, we check the ACF plot and obtain the estimated point at which the correlation diminishes.

The ARMA model integrates features from both AR and MA models, offering a more adaptable and thorough methodology for time-series analysis. The ARMA model with order  , represented as ARMA(

, represented as ARMA( ), is defined as:

), is defined as:

(14)

(14)

where an ARMA model proficiently models long-term dependencies via its AR components and addresses short-term disturbances through its MA components.

In financial time-series analysis, precise forecasting is important for informed investment choices and the formulation of effective trading strategies. AR, MA, and ARMA models provide systematic ways to predict future price movements based on historical data. An AR model can forecast future stock prices by considering the past price movements, while an MA model can evaluate the impact of past market shocks on future prices. ARMA models are often used to estimate future volatility, an essential component of pricing derivatives and constructing risk-hedging strategies.

Given that the aforementioned models are linear, they should always serve as a benchmark before testing any of the more complex, nonlinear deep learning models that are described in later sections. Linear models also have the added benefit of being easy to interpret. This helps form a better intuition for any investment ideas, before moving to more powerful but less interpretable deep learning models.

2.7 Extras

Alpha and Beta

In quantitative finance, the notions of alpha and beta are very important to understanding and evaluating the performance of investment strategies. These metrics are derived from the Capital Asset Pricing Model (CAPM) and are used to measure the returns and risk associated with individual assets or portfolios relative to a benchmark, typically a market index. In quantitative trading, where strategies are often driven by mathematical models and algorithms, alpha and beta provide essential insights into the effectiveness and characteristics of trading approaches.

Alpha assesses an investment’s performance relative to a benchmark index. More specifically, it represents the surplus return that an investment or portfolio achieves beyond the expected return predicted by the CAPM. In other words, alpha signifies the additional value that a trader or investment strategy contributes over what is anticipated based on the asset’s systematic risk. Conversely, beta measures an investment’s responsiveness to market fluctuations. It quantifies the relationship between the investment’s returns and those of the overall market or benchmark, indicating the extent to which the investment’s returns are expected to vary in reaction to changes in the market index. Mathematically, we define alpha ( ) and beta (

) and beta ( ) as:

) as:

(15)

(15)

where  is the return of the investment,

is the return of the investment,  is the risk-free rate and

is the risk-free rate and  is the return of the market. A positive alpha signifies that the investment has surpassed the benchmark, whereas a negative alpha indicates underperformance. In quantitative trading, generating alpha is the primary goal as it reflects the ability of a trading strategy to consistently beat its benchmark through superior stock selection, timing, or other factors. Beta values have different meanings. A beta exceeding 1 signifies that the investment is more volatile than the market, indicating it tends to amplify market movements in response to changes. Conversely, a beta below 1 indicates that the asset’s returns are less sensitive to market movements than the market index itself. If an investment has a negative beta, it means that the investment moves inversely to the benchmark. We can also think of beta as the covariance between strategy and market returns scaled by the market’s variance.

is the return of the market. A positive alpha signifies that the investment has surpassed the benchmark, whereas a negative alpha indicates underperformance. In quantitative trading, generating alpha is the primary goal as it reflects the ability of a trading strategy to consistently beat its benchmark through superior stock selection, timing, or other factors. Beta values have different meanings. A beta exceeding 1 signifies that the investment is more volatile than the market, indicating it tends to amplify market movements in response to changes. Conversely, a beta below 1 indicates that the asset’s returns are less sensitive to market movements than the market index itself. If an investment has a negative beta, it means that the investment moves inversely to the benchmark. We can also think of beta as the covariance between strategy and market returns scaled by the market’s variance.

A strategy that consistently generates positive alpha is considered successful, as it indicates the ability to surpass the market performance on a risk-adjusted basis. On the other hand, beta helps traders understand the risk profile of their strategies and manage risk exposure to market volatility. For instance, a trader seeking to minimize risk might construct a low-beta portfolio, while one aiming for higher returns might opt for higher-beta assets. By utilizing alpha and beta metrics, quantitative traders can make well-informed decisions and enhance their trading performance.

Volatility Clustering

Volatility clustering is an extensively observed phenomenon in financial markets, characterized by sequences of high volatility periods that are succeeded by similarly high volatility periods, and periods of low volatility that are followed by similarly low volatility periods. This characteristic implies that volatility is not constant over time but instead exhibits temporal dependencies, forming clusters. This is one of the reasons why financial returns deviate from the normal distribution. This observation is known as heteroskedasticity and describes the irregular pattern of the variation of a process.

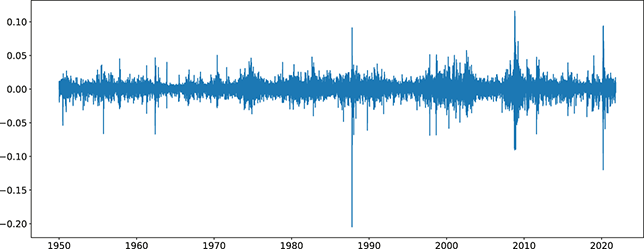

Figure 3 shows the returns of the S&P 500, and we can clearly see that large returns tend to cluster. This means that large fluctuations in prices tend to occur together, persistently amplifying the amplitudes of price changes. Such behavior contradicts the assumption of constant variance in traditional models like the classical linear regression model and calls for models that can accommodate changing variances, in order to make reliable predictions.

Figure 3 Returns of the S&P 500 over 60 years.

There are two popular models used to capture and analyze volatility clustering: the Autoregressive Conditional Heteroskedasticity (ARCH) model and the Generalized Autoregressive Conditional Heteroskedasticity (GARCH) model. These models help in capturing the changing variance over time and provide a better fit for the distribution of returns. Instead of predicting returns  , we now model the variance of returns. An ARCH(

, we now model the variance of returns. An ARCH( ) process of order

) process of order  is defined as:

is defined as:

(16)

(16)

where the variance of the process at time  is determined by observations from the earlier time step. Accordingly, the ARCH model allows for fluctuations in conditional variance over time, effectively capturing volatility clustering.

is determined by observations from the earlier time step. Accordingly, the ARCH model allows for fluctuations in conditional variance over time, effectively capturing volatility clustering.

The GARCH model extends the ARCH model by including past conditional variances into the model, providing a more flexible and parsimonious model for capturing volatility dynamics. We denote a GARCH( ) as:

) as:

(17)

(17)

where the GARCH model presents a dual dependence that is better at modeling both short-term shocks and sustained persistence in volatility over time.

In practical terms, volatility clustering means that markets experience periods of turmoil and periods of calm. ARCH and GARCH models offer powerful methods for analyzing this phenomenon, enabling more accurate forecasting, risk management, and pricing of financial instruments. By recognizing the temporal dependencies in volatility, these models enable us to better understand market behavior and enhance decision-making in various financial applications.

3 Supervised Learning and Canonical Networks

In this section, we explore the essential concepts of supervised learning, an important subset of machine learning that identifies relationships between input data and output labels using example input-output pairs. Supervised learning is extensively applied in a variety of domains, including image recognition, natural language processing, financial forecasting, and medical diagnosis. By mastering the fundamentals of supervised learning, we can proficiently train models to generate accurate predictions and make informed decisions based on new, unseen data.

Supervised learning entails training a model on a labeled dataset, in which each input is paired with its corresponding correct output. The model then learns to associate inputs with outputs by minimizing the discrepancy between its predictions and the actual results. This methodology includes choosing suitable algorithms, adjusting hyperparameters, and assessing the models’ effectiveness. In this section, we will examine these concepts comprehensively, establishing a robust foundation for comprehending and implementing supervised learning methodologies.

Additionally, we will introduce various neural network architectures, which have become the cornerstone of modern machine learning. Neural networks, modeled after the architecture of the human brain, are composed of interconnected layers of nodes (neurons) that process and transform input data. We will cover canonical neural network models, including feed-forward neural networks and state-of-the-art networks such as transformers, each designed for specific types of data and tasks.

Upon finishing this section, you will have a detailed understanding of the core concepts underpinning supervised learning and will better understand various types of neural networks. This knowledge will equip you with the skills to apply these powerful techniques to a wide range of applications, unlocking new possibilities in data analysis, prediction, and decision-making.

3.1 Supervised Learning: Regression and Classification

Supervised learning is at the core of machine learning and it is a process that essentially learns, or in other words, fits a mapping between an input and an output. Formally, for a regression task, it maps an input  to an output

to an output  through a learned function by training on example input-output pairs. We call this collection of example input-output pairs upon which the model is fitted the training set, and it can be expressed as:

through a learned function by training on example input-output pairs. We call this collection of example input-output pairs upon which the model is fitted the training set, and it can be expressed as:

(18)

(18)

A supervised learning algorithm infers a function  that best defines the interplay between inputs and outputs by utilizing training data. The inferred function can then be used to make estimates for new inputs. The function

that best defines the interplay between inputs and outputs by utilizing training data. The inferred function can then be used to make estimates for new inputs. The function  can be as simple as a linear function or it can also be a highly nonlinear function as obtained through deep learning models. During training, the true output values (labels) are available, and our goal is to reduce the differences between the predicted results and these actual labels. In mathematical terms, this reads:

can be as simple as a linear function or it can also be a highly nonlinear function as obtained through deep learning models. During training, the true output values (labels) are available, and our goal is to reduce the differences between the predicted results and these actual labels. In mathematical terms, this reads:

(19)

(19)

where  is a choice of metric, known as a loss function or an objective function, that measures the difference between real outputs (

is a choice of metric, known as a loss function or an objective function, that measures the difference between real outputs ( ) and predicted values (

) and predicted values ( ). After learning a functional mapping on the training set, we apply it to unseen test data

). After learning a functional mapping on the training set, we apply it to unseen test data  and evaluate the performance of our learned function. In general, a supervised learning problem goes through the following steps:

and evaluate the performance of our learned function. In general, a supervised learning problem goes through the following steps:

1. Define the prediction problem,

2. Gather a training set that is representative of the application domain,

3. Carry out an exploratory analysis and select input features,

4. Choose the approximate learning algorithm and decide the model’s architecture,

5. Conduct model training on the training set and optimize hyperparameters using a separate validation set,

6. Assess the effectiveness of the trained function using a test dataset.

Depending on outputs  , we can divide supervised learning algorithms into two categories: regression and classification. When the output (

, we can divide supervised learning algorithms into two categories: regression and classification. When the output ( ) takes continuous values, it is a regression problem. For example, stock prices and the weights and heights of a person are all examples of continuous values that would correspond to a regression task. A classification problem deals with discrete outputs, such as whether an image contains a dog or not. The training framework for regression and classification is very similar, with the exception of the design of the objective function. We now discuss each problem type in detail.

) takes continuous values, it is a regression problem. For example, stock prices and the weights and heights of a person are all examples of continuous values that would correspond to a regression task. A classification problem deals with discrete outputs, such as whether an image contains a dog or not. The training framework for regression and classification is very similar, with the exception of the design of the objective function. We now discuss each problem type in detail.

Regression

One key aspect of supervised learning is the selection of an appropriate loss function – also referred to as a cost or objective function – that measures the discrepancy between a model’s predictions and the corresponding true target values. The loss function guides the learning process by providing a measure that the model aims to minimize during training. As previously noted, regression problems focus on the prediction of a continuous variable. For regression problems, one of the most commonly used objective functions is the mean-squared error (MSE):

(20)

(20)

where the loss is merely the sum of residuals,  , squared which we aim to minimize to obtain a good fit to the data.Footnote 5 The MSE loss is symmetric and places greater emphasis on larger errors in the dataset.

, squared which we aim to minimize to obtain a good fit to the data.Footnote 5 The MSE loss is symmetric and places greater emphasis on larger errors in the dataset.

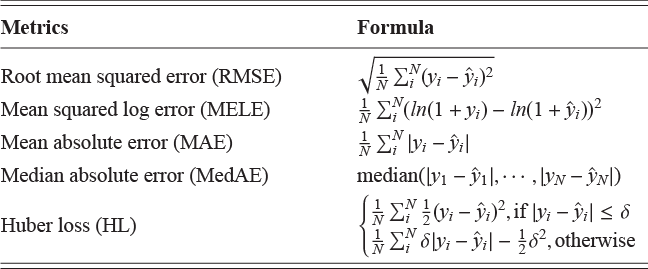

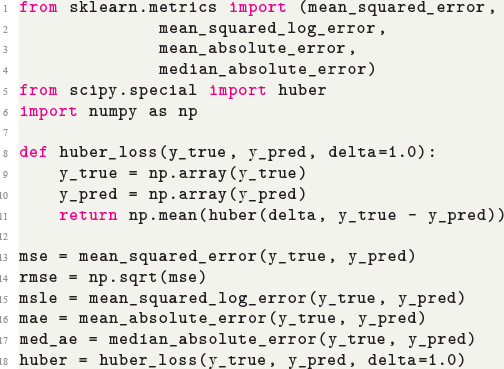

There are numerous options for objective functions. For example, the mean-squared logarithmic error can be applied to outputs that exhibit exponential growth, imposing an asymmetric penalty that is less harsh on negative errors than on positive ones. Both the mean absolute error (MAE) and the median absolute error (MedAE) are symmetric and do not assign additional weight to larger errors. Moreover, Huber loss, which merges aspects of the mean squared error and the mean absolute error, is resistant to outliers and can be used to stabilize training when working with noisy data. Table 1 summarizes some common loss functions for regression problems. It is also very straightforward to implement these losses:

Table 1Long description

The table consists of two columns Metrics and Formula. It reads as follows: Row 1. Root mean squared error (RMSE); root of 1 divided by N summation subscript i and superscript N (y subscript i minus y cap subscript i) the whole square. Row 2. Mean squared log error (MELE); 1 divided by N summation subscript i and superscript N (ln (1 plus y subscript i) minus ln (1 plus y cap subscript i)) the whole square. Row 3. Mean absolute error (MAE); 1 divided by N summation subscript i and superscript N modulus of y subscript i minus y cap subscript i. Row 4. Median absolute error (MedAE); median (modulus of y subscript i minus y cap subscript i to modulus of y subscript N minus y cap subscript N). Row 5. Huber loss (HL); 1 divided by N summation subscript i and superscript N 1 by 2 (y subscript i minus y cap subscript i) the whole square, if modulus of y subscript i minus y cap subscript i less than or equals delta and 1 divided by N summation subscript i and superscript N delta modulus y subscript i minus y cap subscript i minus 1 by 2 delts square. otherwise.

Code 1.3

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

The best choice of objective function depends on the specific task. Sometimes, we can create customized loss functions to ensure that performance metrics best reflect the consequences of incorrect predictions. For example, in applications like medical diagnosis or fraud detection, false negatives may be more costly than false positives. In such cases, loss functions can be tailored to penalize certain types of errors more severely, aligning the model’s training with the specific needs of the problem.

Classification

Unlike regression, classification aims to place input data into predefined categories or classes. It does so by analyzing a labeled dataset where each example is matched with a class label. Once trained, a classification model can predict labels for unseen data based on the learned patterns and relationships. Classification techniques are commonly applied in fields such as finance, healthcare, and marketing. Classification problems can be broadly categorized into binary classification and multi-class classification. Binary classification involves two distinct classes. Common examples of binary classification include determining whether an email is spam, predicting if a credit card transaction is fraudulent, or diagnosing a patient as healthy or ill. Multi-class problems involve more than two classes, such as classifying handwritten digits (0–9), categorizing types of flowers (e.g., the Iris dataset), or classifying news articles into different topics.

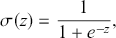

Since classification problems have discrete outputs, we first have to produce scores, or logits, to indicate the likelihoods that an observation belongs to certain classes. These scores can then be normalized across all possible class labels to obtain corresponding probabilities  . After that, we use these scores or probabilities

. After that, we use these scores or probabilities  to make actual predictions

to make actual predictions  either by taking the class with the highest score or by using threshold values. In the simplest case of a binary classification problem, we first define the logistic function

either by taking the class with the highest score or by using threshold values. In the simplest case of a binary classification problem, we first define the logistic function

(21)

(21)

which squashes any real-valued input into the open interval (0,1). We can then model the probability of the prediction being positive as

(22)

(22)

The same mapping can be represented by

(23)

(23)

where the logit of the probabilities is a linear function of input features ( ). The objective functions for classification problems are different from regression as there are instead finite distinct outcomes. In most cases, we choose cross-entropy loss as the objective function for classification. In the binary case, the cross-entropy is calculated as:

). The objective functions for classification problems are different from regression as there are instead finite distinct outcomes. In most cases, we choose cross-entropy loss as the objective function for classification. In the binary case, the cross-entropy is calculated as:

(24)

(24)

where  is the probability of predicting

is the probability of predicting  . The loss function is then computed by summing the cross-entropy of each data point:

. The loss function is then computed by summing the cross-entropy of each data point:

(25)

(25)

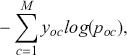

The functional form of the cross-entropy loss might be less intuitive than the MSE, but it can still be understood within the context of maximum likelihood estimation.Footnote 6 If we deal with a multi-class classification problem ( ), a separate loss is needed for each class label and a summation is taken at the end:

), a separate loss is needed for each class label and a summation is taken at the end:

(26)

(26)

where  is a binary indicator (0 or 1) that is activated when the model assigns the right label

is a binary indicator (0 or 1) that is activated when the model assigns the right label  for observation

for observation  , and

, and  is the output from the algorithm which indicates the predictive probability of observation

is the output from the algorithm which indicates the predictive probability of observation  for class

for class  . The loss of the data is then obtained by summing the multi-class cross-entropy of each point.

. The loss of the data is then obtained by summing the multi-class cross-entropy of each point.

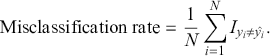

Once the predicted probabilities are transformed into predictions of one class or another, we can evaluate model performance through several metrics. To illustrate those metrics we focus on binary classification problems for simplicity. A frequently employed measure is the misclassification rate which can be defined as the fraction of misclassified labels:

(27)

(27)

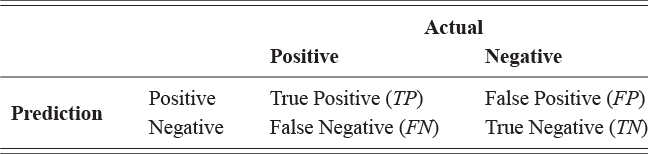

The confusion matrix is another important tool that can be used to visualize various metrics. Table 2 illustrates a confusion matrix that enumerates the quantities of correct and incorrect predictions for every class. For example, the False Positives in the top right corner represent errors where an actual label is negative but a prediction is positive. In the context of a stock price reversion example, this would be a case when a stock price does not revert but we predicted that it would revert. Such an error is much more costly to us than a False Negative, where a stock does actually revert but we predicted it would not.

Table 2Long description

The table consists of three columns blank, Actual: Positive, and Actual: Negative. It reads as follows. Row 1. Prediction: Positive; True Positive (TP); False Positive (FP). Row 2. Prediction: Negative; False Negative (FN); True Negative (TN).

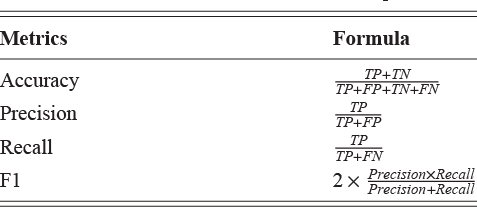

Following the notation in the confusion matrix, we can thus introduce other popular evaluation metrics, which are shown in Table 3. For instance, accuracy is computed by summing the diagonal entries in the confusion matrix and then dividing by the total number of predicted samples. Accuracy thus represents the proportion of total predictions that are correct. Precision indicates the fraction of predicted positives that are truly positive, while recall measures the fraction of actual positives correctly identified. Lastly, the F1 score balances precision and recall by using their harmonic mean.

Table 3Long description

The table consists of two columns Metrics and Formula. It reads as follows. Row 1. Accuracy; True Positive plus True Negative the whole divided by True Positive plus False Positive plus True Negative plus False Negative. Row 2. Precision; True Positive divided by True Positive plus False Positive. Row 3. Recall; True Positive divided by True Positive plus False Negative. Row 4. F1; 2 multiply Precision multiply recall the whole divided by precision plus recall.

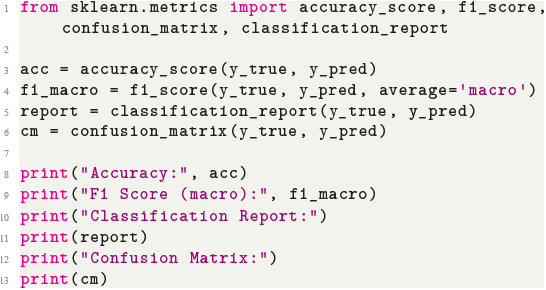

It is very important to check all evaluation metrics when analyzing model performance since a single performance metric can indicate misleading results. For example, in an unbalanced data set, where 90% of labels are +1, we can get an accuracy score of 90% by simply predicting everything as +1, even though the model has not learned anything. Another issue arises when we assign different importance to different types of errors. For example, a mean reversion strategy usually makes frequent small gains but can make infrequent large losses when a stock does not revert. Such a strategy might demonstrate a high accuracy for predicting stock reversion but still lead to significant losses. To implement these metrics, we can use the following code:

Code 1.4

1

2

3

4

5

6

7

8

9

10

11

12

13

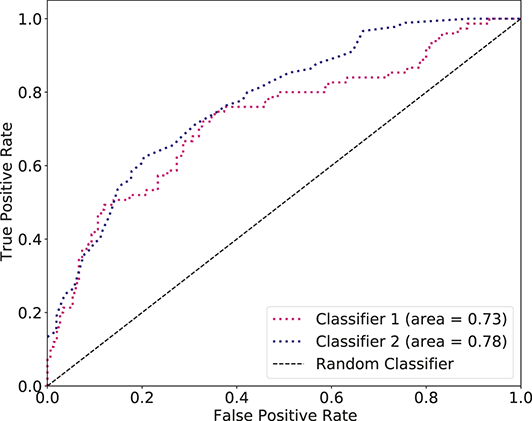

Instead of using numerical values to assess model performance, we can also use graphical tools. The receiver operating characteristics (ROC) curve enables us to compare and choose models that are conditioned on their respective predictive performance. For this purpose, we need to compare predicted probabilities with selected thresholds to decide final outcomes. Accordingly, different thresholds yield different results. The ROC curve derives pairs of true positive rates (TPR) and false positive rates (FPR) by examining every possible threshold for classification, and then displays these pairs on a unit square plot. We define TRP and FPR as the following:

(28)

(28)

Random predictions, on average, yield a diagonal line on the ROC curve which has equal TPR and FPR rates. This diagonal line is the benchmark case, so if the curve falls on the left side of the diagonal line, the learned model is better than random guessing. The further from the margin, the better the classifier (shown in Figure 4). We refer to the area under the ROC curve as AUC and it is a summary measure that tells how good a classifier is. A higher AUC score indicates a better algorithm.

Figure 4 An example of different ROC curves.

Figure 4Long description